Why women aren’t winning in the pension stakes and how to help

By Kim Brown, Pension Scheme Director, Legal & General Mastertrust and IGC

Despite the improvement automatic enrolment has made in increasing participation in pensions, there’s still a huge disparity when it comes to how much money women can expect to retire on compared with men.

The first reason for this is, simply, that women still get paid less than men.

Positive societal changes continue but we’ve a long way to go until we see equality in pay and while improvement has been demonstrated in a relatively (!) quick time in terms of gender equality, the pay gap for those from ethnic minorities or LGBT communities are often further behind and, currently, less well understood.

I look forward to, and actively work towards, a diverse, inclusive and equal workplace. In that future, we can take a gender-neutral approach to overseeing pension savings. Until that time, what can we do to support members who may not be saving enough towards retirement?

When planning for key life events, many people are relatively comfortable with looking at the implications from every angle. Take starting a family, for instance: prospective parents will plan the leave they’ll take, the tiny adorable outfits they’ll buy, and how they’ll budget for the various different gadgets the new family member may require! But the long-term impact on the primary care giver’s later earnings and pension savings is often overlooked.

Even in 2021, women are more likely to be that primary care giver and will often take a career break to do so. Women are also more likely to take leave to care for a loved one, such as an elderly parent, which can result in them having to reduce their hours in paid work or leave work entirely. Such unpaid caring responsibilities along with parental responsibilities are recognised as key factors in the gender pension gap.

On International Women’s Day, it’s important to stress the importance of taking longer-term savings into account when making these life decisions – and employers should do what they can to encourage scheme members to consider the impact on their workplace pensions.

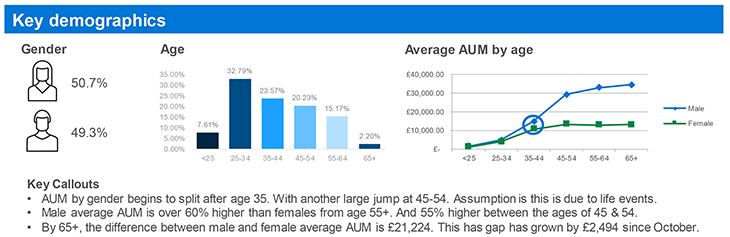

Illustrating the problem

What can be done about it?

Ongoing changes to social and workplace attitudes should help even the gender balance in terms of caring responsibilities alongside the arrival of more flexible working patterns for everyone. That's a gradual process but one that increased state and employer support could expedite.

Meanwhile, there’s much that employers can do to help level the playing field. For example, by considering the gaps in pay within their organisations and seeking to address these imbalances as soon as possible.

Employers could also consider sharing the messages below with their employees and encourage them to use the tools available to help plan for retirement and find out if they’re saving enough to meet their post-work expectations.