Understanding bonus sacrifice

If you get a bonus, sacrificing some or all of it into your pension might not be your first thought. But here’s why it could make sense:

- It’s tax efficient – there’s no tax or National Insurance (NI) due on bonuses that are sacrificed, meaning you can boost your pension by more

- Help grow your pension savings - the more you save, the greater the potential for future growth

- An extra boost – some employers will pass on some or all of the NI savings they make on to you

You’ll be able to access it when you reach the Normal Minimum Pension Age (NMPA). That’s currently 55 but will increase to 57 from April 2028.

How to get started

You can find out more and make your bonus sacrifice between 2 March 2026 and 17 March 2026 on the intranet.

How much tax will I pay on my bonus?

It only takes a minute or so to work that out with our bonus tax calculator.

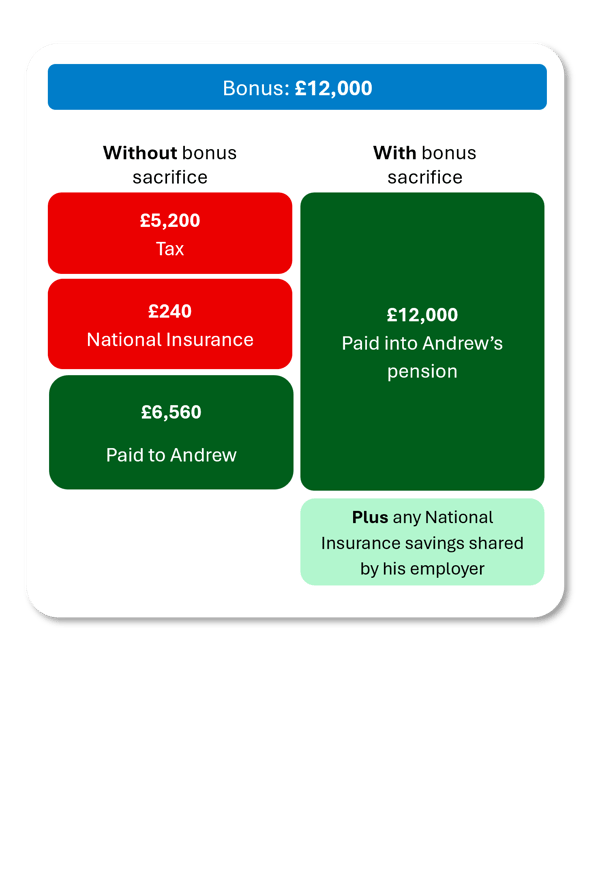

How Andrew invested his bonus

Take Andrew, as an example. Andrew earns £90,000 a year and gets a £12,000 bonus.

If he takes the bonus as cash, he’ll pay higher‑rate tax and National Insurance (NI) on it.

- That will leave him with just £6,680 in hand.

Because his total income is above £100,000, his personal allowance is also reduced. That increases the tax he pays on his bonus.

If Andrew invests the £12,000 bonus in his pension, he doesn’t pay income tax and employee NI.

- The full £12,000 will go straight into his pension.

His employer might also share the NI it saves on the payment, adding it to his pension.

Making sure Andrew doesn’t lose his tax-free childcare

Andrew has two children, one in nursery and one in primary school. Putting his bonus into his pension helps Andrew keep his adjusted net income below the £100,000 threshold, and his partner also has an adjusted net income of less than £100,000. That means:

- He stays eligible for 30 hours funded childcare (from the term after a child turns 9 months, in England).

- He can continue to use Tax‑Free Childcare (a 20% government top‑up via his childcare account).

Adjusted net income is your total taxable income for the year, minus certain tax reliefs (like pension contributions made through bonus sacrifice). It includes things like savings interest, rental income, and dividends.

If your adjusted net income goes over £100,000, your tax-free personal allowance (£12,570 for most people) is reduced – and lost completely once your income reaches £125,140.

How bonus sacrifice can help:

By sacrificing some or all of your bonus into your pension, you may be able to reduce your adjusted net income. This could help you keep your full personal allowance and stay eligible for benefits like tax-free childcare.

If you’re close to the £100,000 threshold, it’s a good idea to check your total income or speak to an adviser.

If you’re a high earner, your annual pension allowance may be reduced – this is called the “tapered annual allowance”.

For tapered annual allowance, you’re considered a high earner if:

- Your “threshold income” is over £200,000, and

- Your “adjusted income” is over £260,000 in a tax year.

For every £2 your adjusted income goes over £260,000, your annual allowance reduces by £1.

- The minimum annual allowance you can have is £10,000 (for those with adjusted income of £360,000 or more).

- If you exceed your annual allowance, you may have to pay a tax charge.

Your threshold income - this is your total taxable income (salary, bonus, rental income, dividends, etc.) minus any personal pension contributions.

Your adjusted income - which is your total taxable income plus any employer pension contributions (or the growth in a defined benefit pension).

- Both “threshold income” and “adjusted income” include all your taxable income (salary, bonus, rental income, dividends, etc.).

- “Adjusted income” also includes all pension contributions (including those made by your employer).

Not sure if bonus sacrifice is right for you?

We’re here to help.

Book a free intro call with one of our advisers.

If you decide to go ahead and get advice, your adviser will:

- Take the time to understand your personal circumstances

- Explain how bonus sacrifice works, the pros and the cons

- Make recommendations based on your individual needs, that support your long-term goals

Advice is a paid for service. Your adviser will explain any costs before you decide to go ahead.

Important points to bear in mind

- Limits on tax relief: Pension contributions usually get tax relief, but annual limits apply (including anything your employer pays in). For 2025/26 the standard annual allowance is £60,000. If you’ve taken a taxable income through pension drawdown, or a taxable lump sum, the Money Purchase Annual Allowance applies, it’s £10,000.

- Tapered annual allowance: Higher earners may have a reduced annual allowance. Check if tapering applies to you on GOV.UK.

- Carry forward: If you didn’t use your full standard annual allowance in the last three tax years, you may be able to carry forward unused amounts to increase what you can contribute this year. Carry forward is not available if you are subject to the Money Purchase Annual Allowance.

- As with any investment, the value of your pension can go down as well as up.

- Reducing your adjusted net income by sacrificing your bonus may help you keep your personal allowance or remain eligible for certain benefits, but it depends on your total income from all sources. If you’re unsure, please seek advice.

- Tax rates are different for those living in Scotland

L&G Podcasts

Episode 1

Pensions contributions in your 30s, 40s and 50's

05:09

Episode 2

Pension contributions before you're 35

03:02

Episode 3

Pension contributions as you approach retirement

04:43