What is Life Insurance?

During these uncertain times, there are things you can do to help financially protect your loved one’s future. And we’re here to help.

Think of life insurance like a safety net. It could pay out a cash sum if you were to pass away while covered by the policy or if you were diagnosed with a terminal illness provided life expectancy is less than 12 months.

Life insurance is there to ensure the life you’ve built together goes on. With the rising costs of living and less disposable income for many, life insurance could be more important then ever. From helping to keep the roof over their heads, to paying the ever-increasing bills, life insurance means you can keep providing the things that really matter even after you're gone.

How does Life Insurance work?

You choose the amount of life insurance you need, how long you need it for and whether you want to take out life insurance in joint or single names. For more help, take a look at our life insurance calculator or speak to your financial adviser.

Here's some great reasons to take out cover with us:

This page was last reviewed by our team of financial protection experts on 30 August 2023.

Or call us on 0800 316 5591

8:30am to 8pm Monday to Friday

9am to 1pm Saturday

We may record and monitor calls

Receive a £100 gift card after you take out cover*

Restrictions apply, see www.amazon.co.uk/gc-legal

Life Insurance cover details

What's covered?

Please read the key documents before you apply:

Things you need to know

How much life insurance could you get?

Below are some real life examples of how much life insurance some of our customers who don’t smoke and have good overall health get for £25 a month for a 25 year policy term, which was the average premium and average length of cover our customers bought between Feb 2022 and Jan 2023.

You can get your own personalised quote if you give us some details about you and the cover you need.

These quotes were taken from legalandgeneral.com on 25 August 2023. Decreasing Life Insurance could be cheaper, but this is specifically designed to protect a repayment mortgage.

| Age when cover starts | Life Insurance cash sum payout |

|---|---|

| 20 year old | £1,154,347 |

| 30 year old | £600,636 |

| 40 year old | £217,907 |

| 50 year old | £79,097 |

| 60 year old | £21,416 |

| 70 year old (maximum length of cover is 19 years) | £6,704 |

Life insurance explained

Do I need life insurance?

Whether you need life insurance will depend on your individual circumstances. For example, life insurance can provide peace of mind for people with children, partners or spouses that depend on them financially, as well as people with a mortgage on the family house.

Are you eligible for life insurance?

Most people who apply for life insurance are able to get the cover they need. Just make sure you answer all of the questions truthfully when you apply. You are eligible to apply for life insurance if you are:

- at least 18 years of age

- currently living in the UK and have spent at least 183 days in the UK in the last tax year.

Life Insurance Calculator

How much cover will you need?

Our life insurance calculator is the easiest way to estimate how much cover you may need to financially protect your loved ones.

What type of life insurance do you need?

We offer more than one type of life insurance, to suit different needs.

Life Insurance

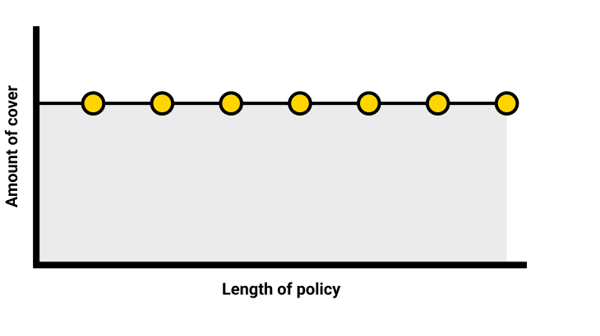

Life insurance, sometimes known as level term life insurance, is where the amount of cover you choose and the premium you pay will stay the same throughout the duration of your policy, unless you decide to make any changes. If you pass away while covered, your family will get a cash sum to help them financially, it could be used to help pay the bills or cover child care costs, for example.

Learn more about different types of life insurance.

Decreasing Life Insurance

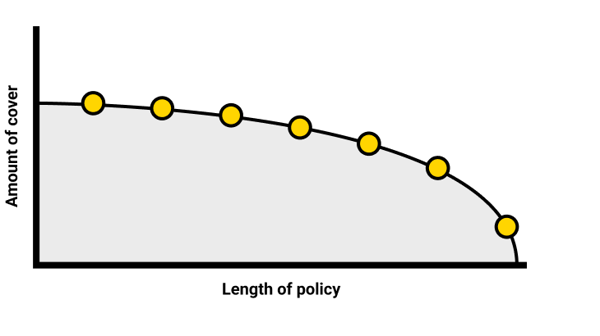

Decreasing life insurance is when the amount of cover you choose will decrease over time, roughly in line with the way a repayment mortgage decreases. This type of life insurance is often taken out to help protect a repayment mortgage. If you were to pass away while covered, your family would get a cash sum to help cover the mortgage, so they get to stay in their family home without the worry of mortgage payments.

Find out more about Decreasing Life Insurance.

Single or joint life insurance?

Single life insurance covers one person, whereas joint life insurance covers two lives. The difference is that joint life insurance pays out upon the death of the first insured person, at which point the cover stops. Some couples prefer to have single life insurance policies, which ensures the surviving partner still has cover after the first death, but joint life insurance policies can be cheaper. Read more about single v joint life insurance policies to work out which is best for your needs.

Why choose Legal & General for your life insurance

The UK's No.1 Life Insurance Provider

*Based on new individual Life Insurance sales in 2022, Term & Health Watch report 2023, Swiss Re.

Award winning cover

**We've been crowned 'Life Insurance Provider of the Year (Direct)' for the 5th time at the 2024 awards.

Expert rated

5 Star Defaqto rated cover, the highest rating possible!

Our Life Insurance claims process

Step 1 - Get in touch

We understand that making a claim is going to be distressing time for your loved ones. That's why our experienced claims staff are specially trained to handle all calls with care and compassion.

Call them on 0800 137 101 between 9am and 5pm Monday to Friday.

Step 2 - Assessment

Our expert claim handlers will deal with the claim as quickly as possible and will keep your loved ones informed throughout the process. They will contact them if they need any further information, such as a claim form or death certificate.

Step 3 - Paying out

If the claim is accepted, we'll pay out within 5 working days directly to the personal representative of the deceased person, usually the executor of the will.

What is Wellbeing Support?

We know that the pressures of everyday life can sometimes be stressful, and can impact your wellbeing in lots of ways. That's why we've introduced Wellbeing Support Service. So whether you need a reassuring chat, some information, or help getting through a challenging time – to name just a few, they are here to help.

Take a look at our dedicated Wellbeing Support hub and find out more.

Care Concierge

If you think that you or someone you know might need care, it can be difficult to know where to start looking or what your options are. Care Concierge is a confidential telephone advisory service that can help you understand and find later life care. Our Care Concierge team have extensive knowledge of the care industry and are completely impartial, allowing you to make an informed decision on the care option that is right for you.

Take a look at our dedicated Care Concierge page to find out more

Our Life Insurance product reviews

As of April 2024, 304 customers have rated our life insurance giving the product an average star rating of 4.4 out of 5 on Trustpilot. The score of 4.4 corresponds to the star label ‘Excellent’. It includes reviews from customers who’ve claimed on a policy.

Related information and products

Life Insurance additional benefits

When you take out our Life Insurance we include a number of additional benefits at no extra cost, such as Free Life Cover and Terminal Illness Cover (where life expectancy is less than 12 months), giving you extra peace of mind. Terms and conditions apply.

Critical Illness Cover

Get extra protection with Critical Illness Cover which can be added for an extra cost when you take out your life insurance policy.

Decreasing Life Insurance

If you're looking for life cover to specifically cover a repayment mortgage, take a look at our Decreasing Life Insurance where the amount of cover reduces roughly in line with the way a repayment mortgage reduces.

Life insurance news and articles

Life insurance calculator

Use our life insurance calculator to help you work out how much cover you might need.

Life insurance news and guides

From information about different types of life insurance to articles about looking after your health and well-being - check out our wide variety of articles and guides.

Making life insurance quotes easy

Getting life insurance quotes is one of those things that probably gets pushed to the bottom of the list. You may think it's going to be too complicated or time-consuming or you simply keep putting it off because it's not something you want to think about.