Reviewed by Lisa Redman on 01 June 2026.

Protect life as they know it

Think of life insurance like a safety net that helps protect your family financially when you’re no longer here. It pays out if you pass away while covered by the policy or are diagnosed with a terminal illness and your life expectancy is less than 12 months. The payout from a life insurance policy can help your loved ones manage outstanding debts such as the mortgage and keep up with the monthly bills and childcare costs.

Getting a life insurance quote online is quick and easy

Or call us free on 0800 316 5591

8:30am to 8pm Monday to Friday

9am to 1pm Saturday

We may record and monitor calls

Life Insurance - uncovered

How does Life Insurance work?

Life Insurance cover details

What's covered

Things you need to know

Policy documents

See a full list of what is and isn't covered in our policy documents before you apply. If you are an existing customer please refer to your policy documents for details of your cover.

£100 gift card

after you take out cover. Restrictions apply - Read more on Amazon

Why choose Life Insurance?

How much life insurance could you get?

Below you can compare how much life insurance our customers can get based on real life examples. This is based on customers who don’t smoke and have good overall health, paying £25 a month for a 25 year policy. This is based on the average premium and average length of cover our customers bought in 2025.

| Age when cover starts | Life Insurance cash sum payout |

|---|---|

| 20 year old | £1,083,422 |

| 30 year old | £563,838 |

| 40 year old | £214,688 |

| 50 year old | £75,521 |

| 60 year old | £23,258 |

| 70 year old (maximum length of cover is 19 years) | £8,645 |

These quotes were taken from legalandgeneral.com on 13 March 2026. Decreasing Life Insurance could be cheaper, but this is specifically designed to protect a repayment mortgage. Get your own personalised life insurance quote today.

How to get a life insurance quote

It takes around 2 minutes to get your personalised life insurance quote. You'll need the following details:

- Your personal details - date of birth, contact details and smoker status.

- Details of the cover you need - what type of life insurance and how much do you need, how long you want cover to last.

- Who do you want to cover - is the life insurance policy for you alone or you and another person.

Why get life insurance with L&G?

We've been protecting families like yours for 190 years. You can trust us to provide expert cover and supporting benefits.

Types of life insurance

We offer more than one type of life insurance to suit different needs.

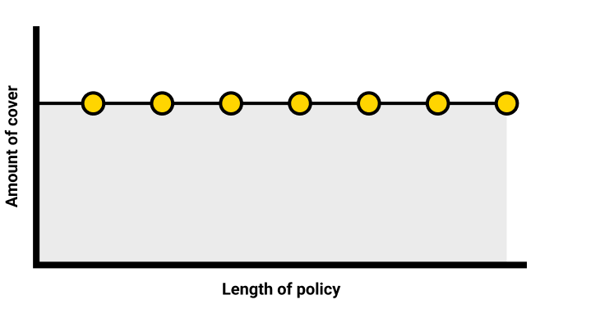

Life Insurance

Life insurance, sometimes known as level term life insurance, is where the amount of cover you choose and the premium you pay will stay the same throughout the duration of your policy, unless you decide to make any changes. If you pass away while covered, your family will get a cash sum to help them financially. It could be used to help pay the bills or cover child care costs, for example.

Learn more about different types of life insurance.

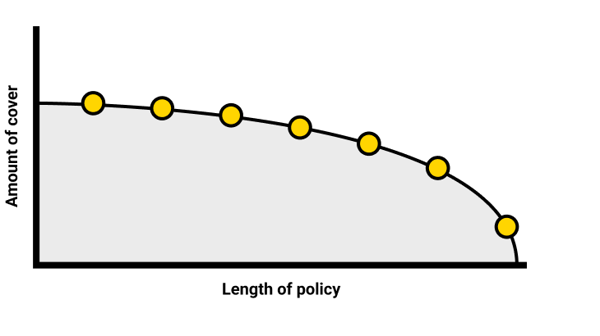

Decreasing Life Insurance

Decreasing life insurance is when the amount of cover you choose will decrease over time, roughly in line with the way a repayment mortgage decreases. This type of life insurance is often taken out to help protect a repayment mortgage. If you were to pass away while covered, your family would get a cash sum to help cover the mortgage, so they get to stay in their family home without the worry of mortgage payments.

Find out more about Decreasing Life Insurance.

Single or joint life insurance?

Not everyone knows the difference between single and joint life insurance, so how do they compare? Single life insurance covers one person, whereas joint life insurance covers two lives. The difference is that joint life insurance pays out upon the death of the first insured person, at which point the cover stops. Some couples prefer to have single life insurance policies, which ensures the surviving partner still has cover after the first death, but joint life insurance policies can be cheaper. Read more about single v joint life insurance policies to compare which is best for your needs.

Our life insurance claims process

Supporting benefits

Related information and products

Life insurance news and articles

Our Life Insurance product reviews

As of 15 May 2026, 1,601 customers have rated our life insurance giving the product an average star rating of 4.4 out of 5 on Trustpilot. The score of 4.4 corresponds to the star label ‘Excellent’. It includes reviews from customers who’ve claimed on a policy.

Our product range