Single vs joint life insurance

When you're comparing single vs joint life insurance, it’s important to understand how each policy works and how a payout could support the people who depend on you. Some couples choose two single policies, others prefer one joint policy, and in some cases a mix of both offers the best fit.

This guide explains the key differences of single and joint life insurance, how each type pays out, and what to think about when choosing the right cover for your situation.

You might also be interested in...

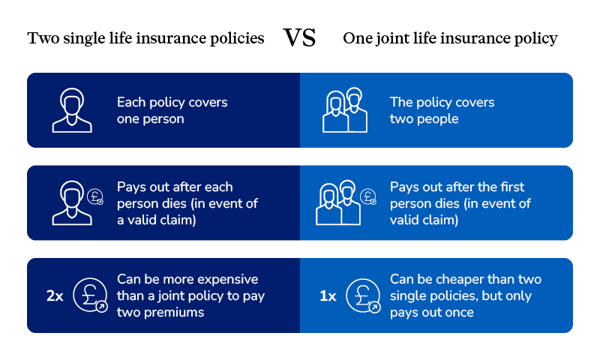

A single life insurance policy covers one person only and pays out the chosen amount of cover if that person dies during the length of the policy. If a couple holds two single policies and one partner dies, then the surviving partner still has their own policy.

A 'joint' life insurance policy covers two lives, which sounds obvious but it’s important to note that the cover usually operates on a 'first death' basis. This means the chosen amount of cover is paid out if the first person dies, during the length of the policy, after which the policy would end. This is a key point about joint life insurance: the policy pays out only once, leaving the surviving partner without cover under that policy.

Joint life insurance for unmarried couples or friends

A life insurance payout is paid to the legal owner (or owners) of a policy, whether you’re married or unmarried. For joint policies, the cash sum is paid to the surviving life insured.

Regardless of your marital status, with L&G you can get a quote for single or joint life insurance.

Some people may think it makes sense for the sole breadwinner of the family to take out a single life insurance policy in their name to protect their family from the possibility of financial hardship if they died. Of course, this ignores the fact that the loss of someone who takes care of the children and the household can also have a huge financial impact on a family.

Nowadays, there are often two breadwinners in the family, so if you decide to take out life insurance it’s even more likely that both partners will need cover. You have options available – single life policies, a joint life policy or a combination of both.

Consider your needs

If you have loved ones who depend on you financially you may have a need for life insurance. Life insurance can be set up on a single life or joint life basis where an insurable interest exists between the applicants. When deciding which of these options is right for you, take stock of your present needs and, though it’s not nice to think about, prepare for worst-case scenarios. You may want to think about the following:

Joint life insurance

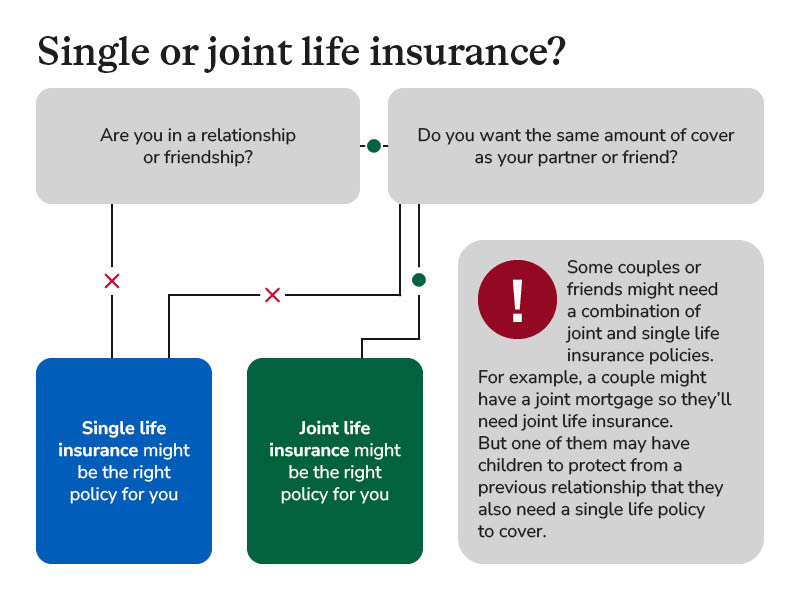

Joint life policies could be a good choice if you both need the same level of cover for the same length of time e.g. to cover a joint mortgage where the cash sum only needs to be paid once if one of you were to pass away while covered by the policy.

Both policy holders would have the same level of cover under a joint life policy, so if you have different protection needs, this may leave one partner with too much or too little protection.

Single life insurance

Single life could be considered if there are differences in the level of cover that you both need, how long you need cover for or whether you want the cash sum paid twice should you both pass away during the length of the policy.

Is joint life insurance cheaper than single?

A joint life insurance policy can be cheaper than two single policies designed to provide the same amount of cover over the same period of time. However, a joint life policy pays out only once in the event of a valid claim being made. This would leave the surviving partner without cover under that policy, whereas single life insurance policies can offer more protection because each partner has individual cover.

How changes in personal circumstances can affect joint life insurance

Your needs may change in the future, it may be a good idea to review or change your cover in order to make sure that you have the correct level of protection in place.

If a relationship breaks down, it's possible that an insurance provider would not be able to divide a joint life policy into two single policies.

If you claimed against a joint life policy, the surviving person would be left without life cover under that policy. Applying for life insurance later in life can be expensive because premiums increase with age. If your health deteriorates it may become more difficult to obtain cover.

As you work through your options, you can get a good idea of how much cover you might need with our Life Insurance Calculator.

Whether you have single or joint life insurance, your policy won’t change automatically after a divorce. If you wish to make changes to your life insurance policy, your decisions may depend on which of the following applies to you.

- If you have a joint life insurance policy, you might be able to split it into two single policies. However, this isn’t always possible, so it’s worth taking a look at your policy documents.

- The ownership of the marital assets, including the family home may change in the divorce settlement.

- If you have single life insurance, you may encounter less financial complications following a divorce, as you can retain your own single policy.

If you have a mortgage life insurance, it could be a good time to review the policy.

For more on this topic, read our guide to life insurance after divorce.

Yes. You can still take out joint life insurance if you’re over 50, depending on the policy type.

Life insurance - covers you if you pass away during the policy term and pays out a cash sum, in the event of a valid claim, to help your loved ones with expenses such as childcare, household bills, or mortgage and rent payments.

Decreasing Life Insurance - designed to help protect a repayment mortgage. The payout reduces roughly in line with the way a repayment mortgage decreases.

Both Life Insurance and Decreasing Life Insurance can be taken out as joint or single policies.

Over 50s Life Insurance can't be taken out on a joint life basis, however each individual can take out their own policy. Over 50s Life Insurance offers guaranteed acceptance for UK residents aged 50–80. You choose an affordable monthly premium to provide a fixed cash sum when you pass away, which could be used for things like funeral costs, small debts, or gifts for family.

Read our guide to life insurance for senior citizens.

Want to learn more about Life Insurance?

Related Articles

Do I need life insurance if I’m single?

Life Insurance Calculator

Life insurance after divorce

Level term life insurance