How to get your family on the property ladder

If you have life insurance, a payout could support your family financially if you were to pass away. But if you’re wondering how to protect your loved ones’ financial future within your lifetime, you may be able to help them get on the property ladder now. We look at whether ‘springboard mortgages’ and gifted deposits can help your nearest and dearest get their first home.

You might also be interested in...

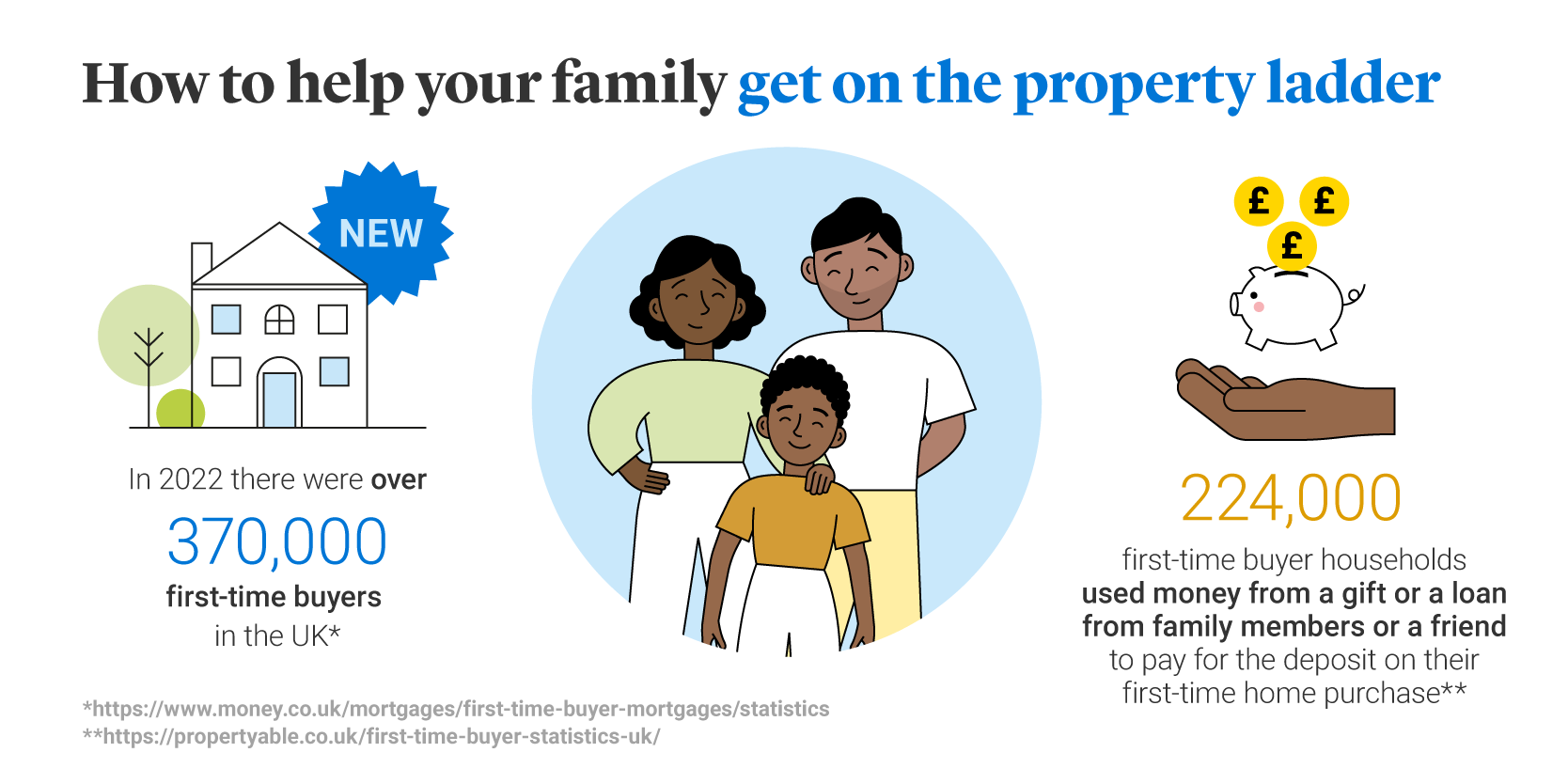

As we all know, getting on the housing ladder isn’t straightforward. According our own research at Legal & General, almost half of under 35s who recently bought a home received financial help from their families in 2024. In this, the average Bank of Family gift or loan was over £27,400. As we’ll explore, for some families, springboard mortgages and gifted deposits could offer a way to fast-track your child, grandchild or other relative’s first property purchase.

What is a springboard mortgage?

A ‘springboard mortgage’ is where you enable someone to buy a property by putting down some of your funds as collateral. It’s called a springboard mortgage because you could help the borrower to ‘spring’ onto the housing ladder thanks to your financial assistance.

How does a springboard mortgage work?

With a springboard mortgage, a friend or family member puts down financial security to help a relative purchase a property, either in the form of equity or funds put into a fixed savings account. This support means that in theory, springboard mortgages can help applicants get on the housing ladder with 0% deposit.

As the helper, you will often need to contribute 10% of the purchase price, which is locked away into the savings account for a defined period – sometimes five years. At the end of this period, you will get your money back as well as any interest accrued.

What are the pros and cons of a springboard mortgage?

A family springboard mortgage might not be the first port of call for every home buyer, but for some, it may be the answer in terms of how to get on the property ladder. Let’s take a look at some of the arguments for and against springboard mortgages.

Pros

Here is how a springboard mortgage can benefit the borrower.

- They can buy without a deposit. On average, home buyers in the UK need to raise £53,414 for a deposit, according to Statista data published in 2023. But with a mortgage deposit from parents, family or friends, they can jump the queue and buy with a small deposit or none at all.

- They can access better mortgage rates. By having a lower loan-to-value (LTV) ratio, the buyer can unlock better mortgage deals and save money in the long run.

- They can get on the ladder more quickly. For a lot of young people, saving for a house deposit can be near impossible. A springboard mortgage can be a huge step in getting on the property ladder and moving away from rented accomodation.

And how do springboard mortgages work in the interests of the family member or friend offering it?

- You can get your cash back. Eventually, once the borrower has continued to pay back the balance over a fixed period of time, for example 5 years, your funds will be released and returned.

- You can earn interest. You can provide an interest-earning contribution towards the springboard mortgage, so it shouldn’t feel like a ‘waste’.

- You can help out a loved one. There are few things more rewarding than being able to help a family member get on the housing ladder and springboard mortgages give you the chance to put any extra cash to good use.

Cons

While there are many benefits of accessing a family springboard mortgage, there are certain things to consider:

- You won’t get your money back if the borrower hasn't made all of their mortgage payments on time.

- Eligibility criteria apply, so age, income or credit history may affect someone’s ability to get a springboard mortgage.

- Springboard mortgages are only for first-time buyers.

- Some lenders will only lend to close family members.

There is more than one way to help a family member get on the property ladder, and next we’ll explore whether gifted deposits are the answer.

What is a gifted deposit?

A gifted deposit is a cash gift that can be put towards a mortgage or to fund a property purchase in full. Unlike a family springboard mortgage, a gifted deposit is not repaid to the gift giver.

How does a gifted deposit work?

According to data from Legal & General Ignite, the free mortgage research and sourcing platform, there has been a notable increase in borrowers turning to family support—dubbed the "Bank of Family"—amid a resurgence in first-time buyer activity.

If you have a family member who’s looking to buy a home you could provide them with a gifted deposit before they purchase their property.

When applying for a mortgage, the applicant should tell their lender and solicitor that the funds include a gifted deposit.

The money is often gifted from a close family member such as a parent, grandparent or sibling. Some lenders may insist that the donor is a close relative, rather than an aunt or uncle, for example

Once you have agreed with the borrower how much money will be transferred, you should write a gifted deposit letter, which includes information such as your name, your relationship to the borrower, the total amount, and confirmation that the money doesn’t need to be repaid.

As the gift giver, you will need to provide proof of your identity and proof of funds as part of the money laundering checks completed by the mortgage provider.

What are the pros and cons of a gifted deposit?

As with springboard mortgages, gifted deposits can help a family member get on the property ladder more quickly. You can also help them access better mortgage rates by reducing their life-time-value (LTV) ratio.

For the gift giver, the main advantage of a gifted deposit is the opportunity to help a loved one at a time when many people are wondering how to get on the property ladder.

But there are other benefits for the borrower:

Pros

- No obligation to repay the money. The borrower won’t need to repay the gift giver as the gifted deposit is not a loan.

- The gifted deposit can be tax-free. If you (the donor) make a gift this is known as a Potentially Exempt Transfer (PET). If you live/survive for seven years the gift will be exempt from your estate for Inheritance Tax (IHT). To find out more about how gifts and Inheritance Tax work, read our guide to life insurance and tax.

- No financial or legal ties. When you provide a gifted deposit, you have no stake in the property, which can help avoid any complications should your child, grandchild or relative wish to sell the property in the future.

For the gift giver, the main advantage of a gifted deposit is the opportunity to help a loved one at a time when many people are wondering how to get on the property ladder.

Cons

- Some lenders don’t accept gifted deposits if the money is not from a close family member.

- Inheritance Tax may be due if you die within seven years following your gift.

- If you’re gifting money to a family member, you will have to think carefully about the long-term financial implications.

- As the gift does not need to be repaid, you lose control of the funds.

Other ways to help your family get on the property ladder

In addition to springboard mortgages and gifted deposits, there are other inventive ways to help a loved one purchase their first property.

For example, you could look into a guarantor mortgage, where a ‘guarantor’ (such as a parent) provides a guarantee that they will pay the mortgage if the borrower does not repay the monthly payments.

If you're considering any of the above its worth seeking mortgage and legal advice before making any decisions.

How life insurance can help homeowners

Finally, once your child or family member has got onto the property ladder, they might want to look into life insurance. Life insurance could pay out a cash sum if the policyholder dies while covered by the policy and the money could be used to help pay off a mortgage. We also offer decreasing life insurance which is designed specifically to help protect a repayment mortgage. With this type of insurance, the amount of cover reduces roughly in line with the way a repayment mortgage decreases.

Want to learn more about Life Insurance?

Other related articles

What's the difference between life insurance and mortgage life insurance?

Life insurance for young adults