Life insurance and tax

We all want to make the best decisions for our loved ones’ financial future. And if you’re thinking about your family’s Inheritance Tax (IHT) implications, a life insurance policy is something you might want to consider.

In this guide we’ll explore how the value of your life insurance might influence your Inheritance Tax planning.

You may also like...

A life insurance payout provides your loved ones with a cash sum which could be used to pay an Inheritance Tax bill without having to sell other assets to meet the cost. Our Whole of Life Protection Plan is available through advisers and can be used to help fund inheritance liabilities.

And by writing your life insurance into a trust, you can protect your beneficiaries from Inheritance Tax.

Your 'estate' describes the total of your assets minus your debts when you die. Inheritance Tax is levied on the value of your estate after death. This includes the value (death benefit) of your life insurance policy.

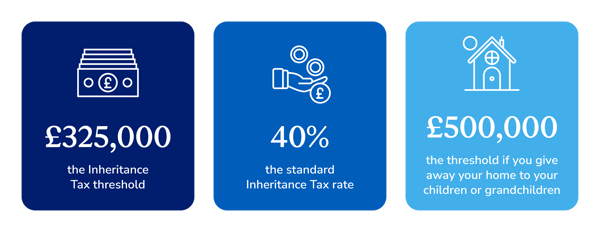

If the total value of your estate (including the life insurance payout) is greater than the Inheritance Tax threshold, then the excess value will be subject to a 40% Inheritance Tax charge. If your policy is in trust however, you can protect your beneficiaries from inheritance tax charges.

What is the Inheritance Tax threshold?

The IHT threshold (the nil-rate band) is currently £325,000 in the UK for individuals or as much as £650,000 for married couples or civil partners.

A life insurance payout is not usually taxable. However, any interest earned on the policy between your death and the payout may be subject to Income or Capital Gains Tax.

If your life insurance policy is written in trust, the payout is not legally part of your estate. Therefore, it’s not subject to IHT, which means your beneficiaries receive the full sum.

It’s advisable to seek advice from a financial advisor to understand how life insurance can align with your overall IHT planning strategy.

The payments you make to an insurer for a policy are called premiums. Your life insurance premiums are not tax deductible. That means for a personal life insurance policy, your premiums will not be considered an allowable expense by HMRC.

While your life insurance premiums are not tax deductible, your policy can be treated as a gift for Inheritance Tax purposes when placed into a trust.

Your estate is subject to taper relief which reduces the amount of tax payable on lifetime gifts; after seven years, there is usually no Inheritance Tax to pay.

Tax relief isn’t available but there are some IHT advantages when you place life insurance in trust.

There can be an immediate IHT charge if you gift some assets to a trust. This doesn’t normally apply to life insurance. This is because you’ll be in good health and the ‘open market’ value of the policy is likely to be negligible.

You’ll be paying for a policy that’s legally owned by trustees. Each premium is technically classed as a gift for IHT purposes. While it’s not tax relief, this series of gifts is normally exempt from IHT. This is because they’re ‘regular gifts made from income’ or they fall under the ‘annual gift allowance’.

Want to learn more about Life Insurance?

Related Articles

How to find lost life insurance

Life insurance when moving abroad

Life Insurance Calculator

What you need to know if you’re a life insurance beneficiary

Benefits of life insurance