What you need to know if you’re a life insurance beneficiary

If you have been named as beneficiary in a life insurance policy of a will or in trust you may be wondering what that means and how it works. We take a look at what a life insurance beneficiary is, and answer some of the key questions you might have.

You may also like...

A life insurance beneficiary is the named person (or people) who may be entitled to inherit a lump sum of money if the life insurance policyholder passes away. This depends on a valid life insurance claim being made during the lifespan of the policy.

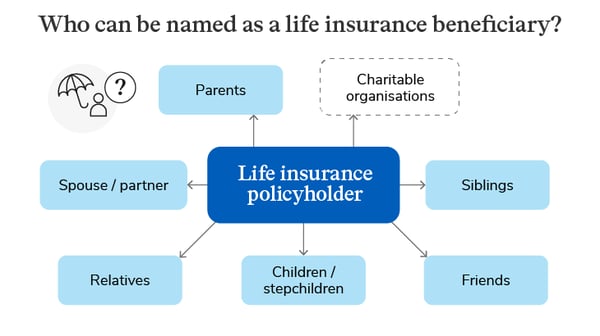

A life insurance policyholder can name anyone as a beneficiary, such as:

- A spouse.

- A common law partner.

- Children/stepchildren.

- Parents.

- Siblings.

- Close or distant relatives.

- Friends.

- Charitable organisations.

Beneficiaries can be named individually or as a group (for example, using the term “my grandchildren”, which covers grandchildren and unborn grandchildren). The beneficiaries of an estate – which includes the value of a life insurance policy – can be named through the insured person’s will. Beneficiaries can also be named when a life insurance policy is placed in trust. If there is no will, the proceeds of the estate will be shared according to the rules of intestacy.

Your will lets you decide what happens to your money, property and possessions after your death. If you make a will you can also make sure you do not pay more Inheritance Tax than you need to. Find out more about life insurance and inheritance tax.

A trust is a legal arrangement which allows the owner of a life policy (the settlor/donor) to give their policy to a trusted group of people (the trustees), who look after it. At some time in the future, they pass it on to some people from a group that the settlor has decided (the beneficiaries). Any assets held in a trust are deemed to be outside of an estate.

The value of your life insurance policy will form part of your estate unless you’ve written your life insurance policy ‘in trust’. If this is the case, the amount the policy pays out wouldn’t be counted as part of your estate for Inheritance Tax purposes.

Yes, but any beneficiary classed as a minor (under 18 years old), can’t receive the money until they’re 18. So for any life insurance policyholder, it’s worth considering what will happen at the claim stage if the beneficiary is yet to reach the age of 18. For example, the beneficiary’s parent or guardian could use the money to help with daily living costs or education.

Life insurance trusts and beneficiaries

There are various ways that a life insurance policy can be placed in trust, and as a beneficiary, you may want to familiarise yourself with these legal arrangements:

An absolute trust.

This is where the owner of a life policy (the donor) gives their policy to a trusted group of people (the trustees), who look after it. The donor chooses the beneficiaries at the outset (and cannot be changed). At some point, the proceeds of the trust will pass on to the beneficiaries.

A discretionary trust.

This is where the trustees have the freedom to choose which beneficiaries to pass the trust onto, how much each beneficiary will get, and when.

A flexible trust.

This is where there are two types of beneficiaries – the ‘default beneficiary’, who is entitled to any income from the trust as it arises, and the ‘discretionary beneficiary’, who only receive capital or income from the trust if the trustees make appointments to them during the trust period. If no appointments are made by the end of the trust period, the default beneficiaries will receive all the benefits.

Changing a beneficiary on a life insurance trust

A life insurance policyholder might decide they want to change the beneficiary of their life insurance. This could be because their relationship with the beneficiary has changed, or perhaps the beneficiary has inherited money from another source and no longer needs it. Either way, it’s often possible to change the beneficiary on a trust, but this depends on the type of trust you have chosen.

How to find out who a life insurance beneficiary is

Ideally, you will have been informed by the policyholder while they’re alive that you’re a named beneficiary in their will, or that the policy was written under trust. If you’re a named beneficiary, the executor of the will (or trustee) may contact you. It may be possible that you are unaware that you are a beneficiary.

If you’re not sure whether you’re a beneficiary – or indeed whether the deceased was even insured – you could start by trying to locate the policy documents (if you’re a close relative or you have permission). If we can’t tell you then the executor or trustee may wish to inform you.

Do life insurance companies contact beneficiaries?

The short answer is no. In the first instance, the executor, trustees of the policy or a family member will usually inform the life insurance company that the policyholder has died. Either way, the executor or trustees would then pass the lump sum on to the beneficiaries.

How is life insurance paid out to beneficiaries?

It’s very rare that a beneficiary receives the money from a life insurance payout directly. There are two ways that the lump sum can be paid. Firstly, following a valid life insurance claim, the payout is paid directly to the legal owner of the policy or their personal representative, which is often the executor of the will. The executors are ultimately responsible for distributing the proceeds of the estate in accordance with the will. If the deceased didn’t leave a will, the lump sum will be paid to the administrators. Secondly, if the policy was written under trust, the money from a payout is paid to the surviving trustees as the legal policy owners, and they would subsequently distribute any funds to the beneficiaries.

As a life insurance beneficiary, you would receive any money once the executor had settled any unpaid debts and taxes from the estate. Read more about how life insurance payouts work.

No, the lump sum from a life insurance payout is paid to the beneficiary (or beneficiaries), who would not be liable for either Income Tax or Capital Gains Tax. However, if the life insurance policy forms part of the policyholder’s estate, it could be subject to Inheritance Tax (IHT) if the total value of the estate exceeds £325,000. If the life insurance policy has been written 'in trust‘, the value of the policy is generally not considered part of the estate, so there may be no IHT liability.

Yes, while the insured person is alive, they can change their will as many times as they like – including information about beneficiaries – as the will comes into effect upon the death of the individual.

A life insurance policyholder chooses the identity of their beneficiary (or beneficiaries) with their insurer when they take out a policy. Even if they alter the name of a life insurance beneficiary mentioned in their will, this won’t supersede the rights of the beneficiaries listed with their insurer.

A will can’t be changed after death, but as we’ll explore later, contesting a life insurance beneficiary is theoretically possible.

No, the beneficiaries named in a will not inherit any debt. However, any amount they receive from the estate will be reduced once funeral costs and debt payments have been settled.

Yes, in theory you can contest the status of a life insurance beneficiary, but this is ultimately something that would need to be settled through a legal process; your insurer will not be able to overturn this on their own.

If the policyholder organised a will before they passed away, they are likely to have stated an exact percentage of the inheritance that each named beneficiary should receive. This means that life insurance can be paid out to multiple beneficiaries. The executor of the will is ultimately the person who will distribute the funds according to the deceased person’s wishes. If there is no will in place, the rules of intestacy take effect, meaning multiple surviving relatives could theoretically receive a life insurance payout. If the policy was written under trust, then the lump sum would be paid to the surviving trustees who would distribute to the beneficiaries.

If a policy is written under trust then this should help ensure that the money paid out from the life policy can be paid quickly to the right people, without the need for lengthy legal processes. This is because the trustees are the owners of the policy placed in trust, so they do not have to go through a long legal process in order to make a claim.

Otherwise, when the policyholder dies, the personal representatives need to obtain probate so that they have the authority to deal with the estate. In England and Wales, either a ‘grant of probate’ or ‘grant of letters of administration’ is issued to the personal representatives. This process takes time and if someone dies without having made a will, it takes even longer.

Find out more about our Life Insurance

Other related articles

How to find lost life insurance

Life insurance and tax

Protecting yourself from life insurance scams

How do life insurance payouts work?