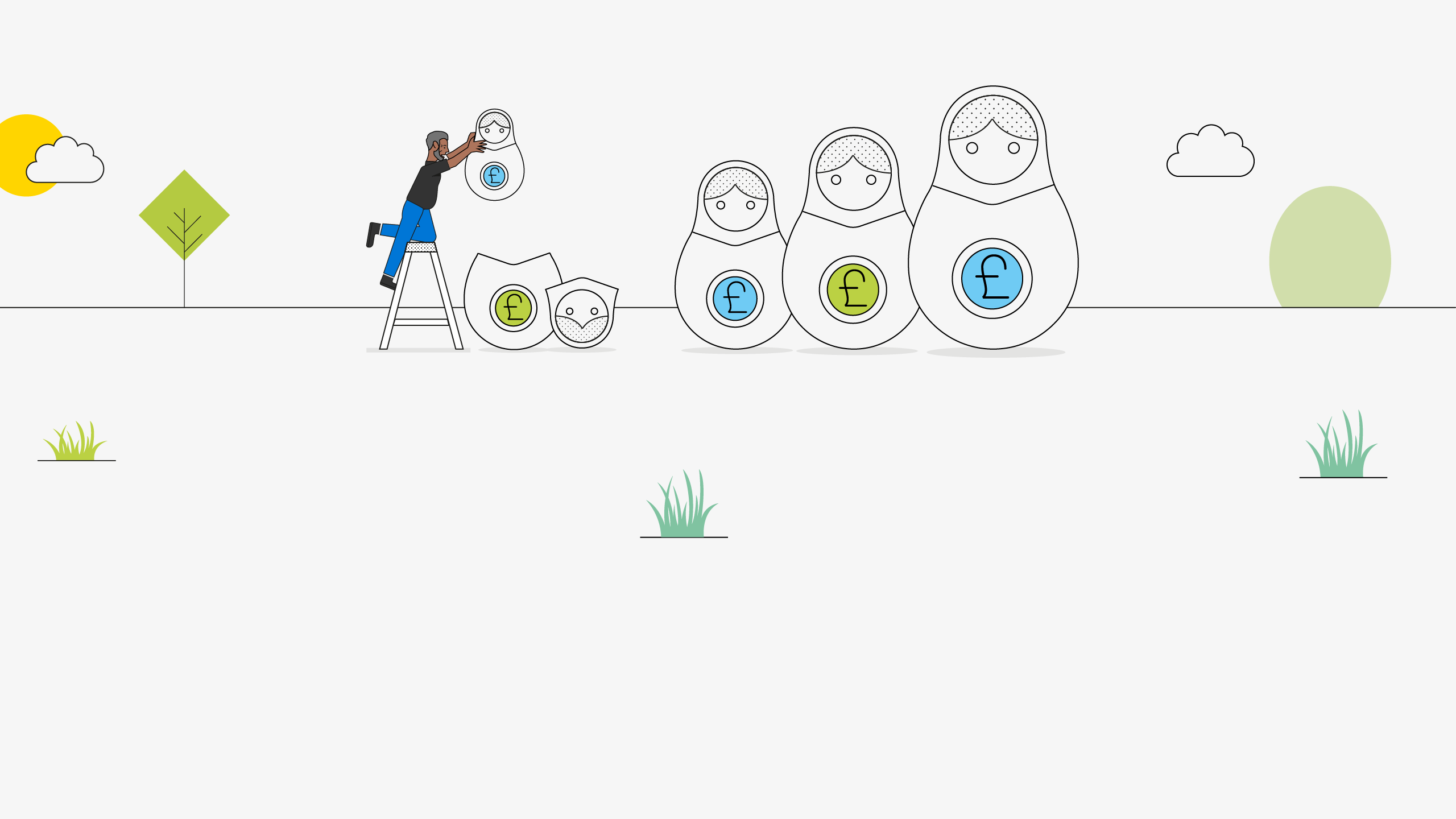

Get all your pensions into one place

If you've got Defined Contribution pension pots with previous employers, you can normally transfer them all into one plan. Keeping your pension savings in one place could make them easier to manage, cost you less and give you greater choice, but it might not be right for everyone.

Things to consider

There are a few things you need to consider before you make a decision about transferring your pots into one place, including:

- the charges for each plan

- whether there are any penalties for transferring

- whether there are any benefits or guarantees you might lose if you move your money

- what options are available at retirement

If you've built up any benefits in a defined benefit scheme, it is usually best to leave these where they are. To ensure that people don't lose out on these valuable pensions by mistake, the government requires anyone who wants to transfer a defined benefit pot of more than £30,000 to take financial advice.

If you are considering transferring your previous plan to Legal & General, we recommend you read the Guide to pension transfers. This guide has a 'transfer checklist' with a range of questions you should consider before deciding to transfer. If you wish to proceed with a transfer, please ask us for a transfer-in application form.

Guide to pension transfers

If you are considering transferring your previous plan to Legal & General, we recommend you read the Guide to pension transfers. This guide has a 'transfer checklist' with a range of questions you should consider before deciding to transfer. If you wish to proceed with a transfer, please ask us for a transfer-in application form.

Getting advice

We would always recommend taking financial advice to make sure that transferring is the right thing for you. You can find an adviser in your local area at unbiased.co.uk. Financial advisers usually charge a fee for their services, but it will be personal to you and your circumstances. You may have the ability to pay your adviser directly from you pot depending on the type of scheme you have. This is called a facilitated adviser charge. The Facilitated adviser charge guide explains how this works.

Finding lost pensions

Private and workplace pensions should send annual statements, but they're easy to lose. If you've lost track, don’t panic; 'lost' pensions are usually the result of when people move home and forget tell a pension provider from a previous job. In some instances, people may not even remember or realise that they were enrolled into an employers' pension scheme.

1.6 million pensions holding an average of £13,000 each have been lost in this way, according to a 2018 estimate by the Association of British Insurers.

If you think you may have had pensions with previous employers or that you set up yourself, you can try to trace them.

You'll need the name of your pension provider or your previous employer to use the service. The service won’t tell you if you have a pension or what its value is. But with the right contact details you can get in touch yourself to find out more.

gov.uk

Use the government's online service to help you get up-to-date contact details so you can find out if you have any entitlements.

Be aware of scams

Pension scams are on the increase in the UK so be aware because a lifetime of savings can be lost in moments.

The Financial Conduct Authority (FCA) and The Pensions Regulator (TPR) say that pension scam victims lose an average of £91,000.

Since 2015 you've had more choices about how you access your pot and scammers will try to lure you with one off deals and guaranteed high returns if you transfer your pots to them. Although there is a cold calling ban in place, they still use this method and they can also use very professional looking websites to get around this. So be on alert.

MoneyHelper has a tool to help you identify a pension scam. Use the Pension Scams tool.

Pension scams tool

MoneyHelper has information to help you identify a pension scam.

MoneyHelper is part of the Money and Pensions Service.