How would you pay your bills if you couldn't work?

For most of us, being unable to work for medical reasons would present a serious financial challenge. What would happen to you or your loved ones if you couldn’t work due to illness or injury which resulted in a loss of earnings? How would you cover your outstanding bills like rent, mortgage or other living costs.

Income protection insurance can give you the peace of mind you deserve. A loss of earnings could have a real financial impact on any family’s lifestyle, and income protection insurance is designed to meet the needs of people who want to protect against this, by paying out a regular monthly amount.

Income Protection Benefit

If you need advice or a wider range of policy options, our Income Protection Benefit is available through our team of expert financial advisers.

Call us today for a quote

9am to 5pm Monday to Friday. We may record and monitor calls.

It would take the average UK earner 10 years to save their gross annual income*. So we can't all rely on savings if we found ourselves unable to work.

What you'll get with Income Protection Insurance

- Regular monthly benefit if you can't work due to incapacity caused by an illness, or an injury which results in a loss of earnings

- Guaranteed premiums unless you make any changes to your plan or if you choose our Increasing Income Protection Benefit plan

- Support with our return to work Rehabilitation Support Service

- Flexibility to make changes such as the benefit amount (eligibility criteria applies)

- Wellbeing Support. We've partnered with RedArc Assured Limited whose registered nurses provide a wide range of phone-based wellbeing services. Find out more.

- Care Concierge Free access to our team of Care Experts, this confidential and impartial telephone advisory service can help you or loved ones understand and find adult and later life care. Find out more.

How our income protection insurance works

Income Protection Benefit

Flexible income protection that helps cover loss of earnings.

- Pays out after a waiting period of 4, 8, 13, 26 or 52 weeks. Pay outs are monthly in arrears

- Covers up to 60% of your gross annual income, up to £60,000 a year. Then 50% of your gross annual income over £60,000 a year. If you need to make a claim, we'll use your income from just before you became sick or injured to work out your monthly benefit.

- Cover can last until your 70th birthday, or your chosen retirement age if earlier.

- You'll receive the monthly benefit until you return to work or your policy ends

- Pay outs are tax free, but could affect a claim for state benefits

This policy does not include unemployment cover so will not pay out if you become unemployed or you're made redundant. It is not a savings or investment plan and has no cash value unless a valid claim is made.

If you are an existing customer please refer to your policy documents for details of your cover.

Get advice

Income Protection Benefit is available from our expert advisers. They can:

- Help if you are unsure about the protection you need.

- Make recommendations for protection to suit your personal circumstances.

- Help you make your application.

Call our team for advice on 0800 294 0275 to talk through your options and to receive a personalised quote to fit your needs.

Financial resilience

The average household is just 19 days from the breadline, far shorter than the 60 days they believe - *Legal & General research

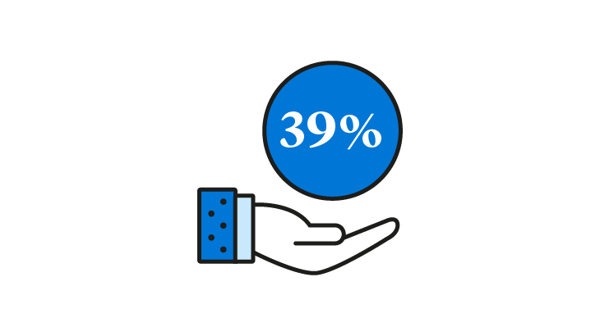

39% of people interviewed are concerned of getting a serious long-term chronic illness, while 8 in 10 are concerned about at least one issue affecting ability to work

The average UK household has £2,431 in savings, but they need around £12k in savings to feel secure.

2 in 5 households have less than £1,000 in savings. In fact 1 in 5 have no savings at all.

What is Wellbeing Support?

The wellbeing of our customers is extremely important to us and that’s where Wellbeing Support comes in. We’ve partnered with RedArc Assured Limited, whose registered nurses can provide you with a wide range of wellbeing services. Here's some quick facts about our Wellbeing Support.

Take a look at our dedicated Wellbeing Support hub and find out more.

Related information and products

Life Insurance additional benefits

When you take out our Life Insurance we include a number of additional benefits at no extra cost, such as Free Life Cover and Terminal Illness Cover (where life expectancy is less than 12 months), giving you extra peace of mind. Terms and conditions apply.

Critical Illness Cover

Get extra protection with Critical Illness Cover which can be added for an extra cost when you take out your life insurance policy.

Decreasing Life Insurance

If you're looking for life cover to specifically cover a repayment mortgage, take a look at our Decreasing Life Insurance where the amount of cover reduces roughly in line with the way a repayment mortgage reduces.