Compare annuities: Should I buy one?

We’ve put this article together to help you decide if an annuity’s a good idea for you. So we’ll be explaining how different types of annuity work. And since people looking at annuities often also ponder annuity or drawdown, we’ll cover that comparison too.

Types of annuity

You can choose between many different types of annuity. We’ve listed them all here, with a link to the relevant product page if we offer that kind of annuity ourselves.

- Lifetime annuities regularly pay out a guaranteed sum of money for the rest of your life. And if a standard one doesn’t meet your needs, you can also get these other kinds:

-

- Joint lifetime annuities regularly pay out a guaranteed sum of money for the rest of your life, then keep paying it to a loved one after you die.

- Fixed term annuities pay out a guaranteed sum of money for a fixed period of time, stopping when that time ends. You can also choose a lump sum payment at the end of it.

- Enhanced annuities give you a better annuity rate if you have certain health or lifestyle issues.

- Immediate needs annuities help you cover care costs by paying a guaranteed sum of money to your care provider for the rest of your life.

- Deferred annuities let you delay the start date of your regular, guaranteed sum of money by a year or more.

- Variable annuities pay out a variable amount of money for the rest of your life, with the exact amount depending on how the investments they’re based on do.

- Purchased life annuities work like other kinds of annuity, except you buy them with a lump sum payment (usually from savings) rather than money from your pension pot.

Want to learn more about annuities?

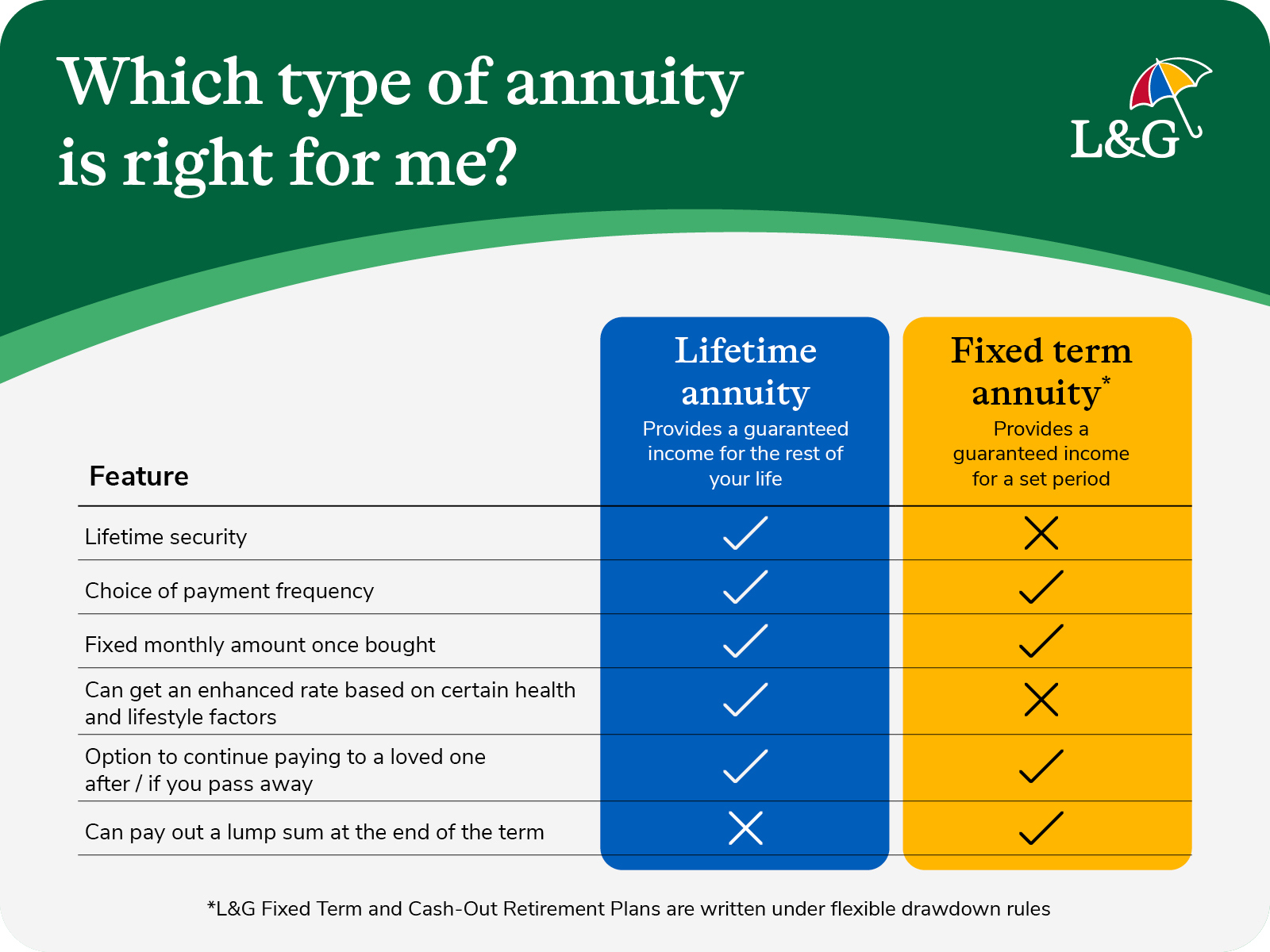

Which type of annuity is right for me?

Annuities provide steady income, but they grow and pay out differently. Here is how lifetime and fixed-term options compare:

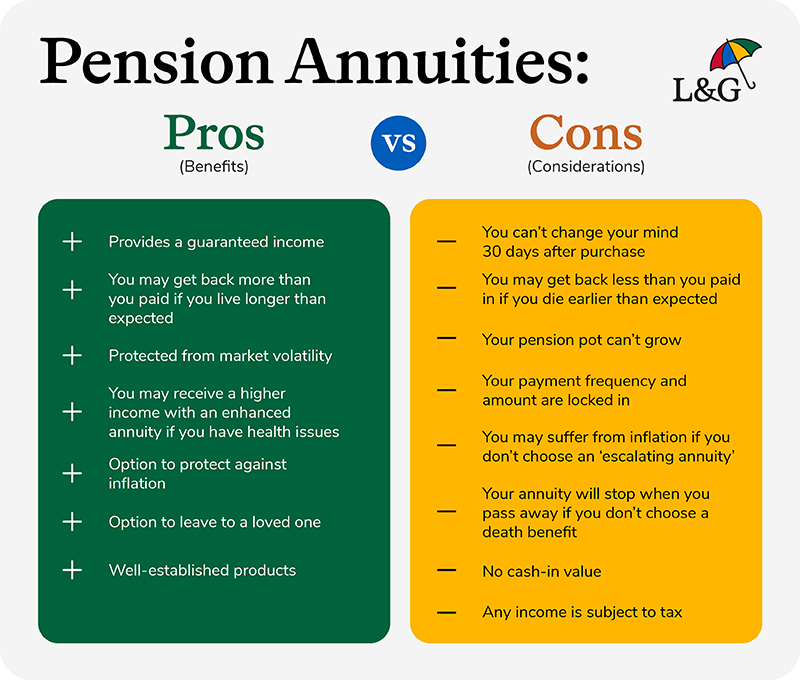

Annuity pros and cons

For many people, the main pro of annuities are that they pay a guaranteed income for life. However a potential con for annuities is that once you've set one up, you can't make any changes to it. Review these pros and cons to see if an annuity could support your retirement plans:

Is an annuity right for me?

That depends on your goals, your circumstances and how much certainty you want from your retirement income.

An annuity isn’t right for everyone — but for some people, it can provide valuable peace of mind.

An annuity could be right for you if:

- you want a guaranteed income you can rely on, especially if you’re worried about economic or market uncertainty

- you’re aged 55 or over and have at least £10,000 to use from your pension pot

- you’re well into retirement or want stability rather than flexibility

They can be particularly attractive if you’re in poor health. Many providers offer enhanced annuities, which pay a higher income to people with common health or lifestyle conditions.

As a general rule, the older you are, the better the annuity rate you’re likely to be offered.

Age can work in your favour — but timing is still a personal decision.

- annuity rates have risen in recent years

- there’s no guarantee they’ll stay at today’s levels

- waiting may mean a higher rate later, but also means delaying certainty

The right time to buy depends on what you need your retirement income to do now, not just what it might do later.

Annuities don’t have to be all or nothing.

Many people choose a blended approach, for example:

- use part of your pension pot to buy a guaranteed or fixed‑term annuity to cover everyday living costs

- keep the rest in drawdown to provide flexibility for one‑off or unexpected expenses

This can help balance certainty with flexibility.

Depending on the options you choose, an annuity can also help you:

- provide an income for a partner or loved one after you’ve gone

These choices usually need to be made upfront, so it’s important to think them through carefully.

Once an annuity is set up, you usually can’t make changes to it. Before committing, it’s important to check:

- how it fits with the rest of your finances

- whether your annuity income will be taxable

- whether it could affect any means‑tested benefits you receive

It’s also essential to shop around to make sure you’re getting the best deal and understand any fees or costs involved.

An annuity may be less suitable if:

- you’re a younger retiree and don’t need guaranteed income yet

- you value flexibility and control over how and when you take money

- you’re comfortable with investment risk

In these cases, other retirement income options — such as drawdown — may be worth exploring.

If you’re not sure whether an annuity is right for you:

- our deciding how to use your pension pot tool can be a helpful starting point

- If guaranteed income sounds appealing, you may also want to speak to our retirement advice service about how an annuity — on its own or as part of a blended solution — could work for you

Annuity vs drawdown

Putting your pension pot into drawdown means you leave your money invested for you to take out (or ‘draw it down’) as and when needed. The money left invested could grow to replace some or all of the money you draw down, though its value could also drop.

So let’s compare a pension annuity with drawdown. What are the main differences?

| Annuities | Drawdown |

| They’re less flexible, because once they’re set up you can’t change how they pay out. | It’s more flexible, because you can choose when and how much money you take out. |

| They’re more secure, because they give you a guaranteed income for a fixed period or life. | It’s less secure, because your savings could go down in value or just run out. |

| They’re a product you buy, so you can’t reclaim any money you spend on one. | It’s a way of investing your money, so its value might grow and it’s there when you need it. |

| You’ll get a better deal if you’re older or have certain health or lifestyle issues. | Your age, health and lifestyle make no difference to its benefits or costs. |

| If you die sooner than expected, your annuity might cost more than it pays out. | If you die sooner than expected, any money left in drawdown will go to your loved ones. |

Which is better – annuity or drawdown?

That depends on what’s most important to you. As a rule, people choose drawdown products for their flexibility and annuities for their predictability. And it doesn’t have to be an either/or pension drawdown vs annuity choice. More and more people are using both together.

For example, when you retire you might want to guarantee that you can always cover your bills. So you spend some of your pot on an annuity, which gives you a guaranteed income for life. Then you can invest the rest of it however you’d like.

Comparing annuity providers and rates

If you’re thinking about buying an annuity, it’s very important to shop around. That’s because different providers offer different products, benefits and rates. It’s also a good way of making sure you understand how annuities work.

As part of your comparison process, we recommend:

- Being very clear about your financial goals and needs. There’s no such thing as a perfect annuity for everyone. You can only choose the best one for you if you’ve got a clear sense of what it should achieve for you.

- Using our annuity calculator. It will help you understand what sort of rates you could get from us at different ages, and assuming different feature choices. It’s also worth exploring other reputable annuity calculators – just search online for them.

- Getting a quote from us. We will of course tell you about our products, but if you can get a better deal elsewhere we’ll also tell you about that. We want to make sure you find the annuity that’s right for you, whether or not it’s one of ours.

- Getting financial advice. Once you’ve bought an annuity you can’t change it. So it’s very important to make sure that you’re making the right choice for you. An adviser will help with that. And they can manage the annuity-buying process for you too.

FAQs

Annuities are designed for income security; they are not an investment as they don’t maximise growth or returns.

They’re worth it if you value guaranteed income for life and protection from outliving your money.

At retirement, when you want a guaranteed, stable income and protection from market volatility. Annuity rates can also impact the best time to buy an annuity.

Related articles

How much does an annuity cost and how do I buy one?

What are the latest annuity rates?