Self-employed life insurance

There are lots of benefits of being self-employed, from the variety of work to setting your own schedule. But for all the upsides, if you’re self-employed you won’t automatically have the same protections as full-time employees – from paid leave to pension schemes. In this guide, we’ll explore how life insurance can give self-employed people extra certainty and financial peace of mind.

You may also like...

Yes, self-employed people can take out life insurance like any other adult. The purpose of life insurance is to provide a cash sum to your loved ones if you were to die (or be diagnosed with a terminal illness, normally with a life expectancy of less than 12 months) before the end of the policy. For the self-employed, life insurance could provide your family with a financial lifeline.

Life insurance can be beneficial if you’re self-employed.

Being your own boss gives you certain freedoms. But self-employment could mean the loss of occupational benefits employees take for granted.

For example, many organisations offer a ‘death-in-service benefit’ to staff. This is where an employer pays a cash sum if the employee dies while on the payroll. This is a multiple of the employee's salary, paid to the loved ones they've left behind. You won’t receive death-in-service benefit as a self-employed person. So, Life insurance means that if you were to die, your family would have some financial security."

There are also other types of insurance which can mitigate the absence of statutory sick pay.

How does life insurance for self-employed people work?

Life insurance works the same way for our self-employed and employed customers. Here are some of the factors you may want to consider as a self-employed life insurance applicant.

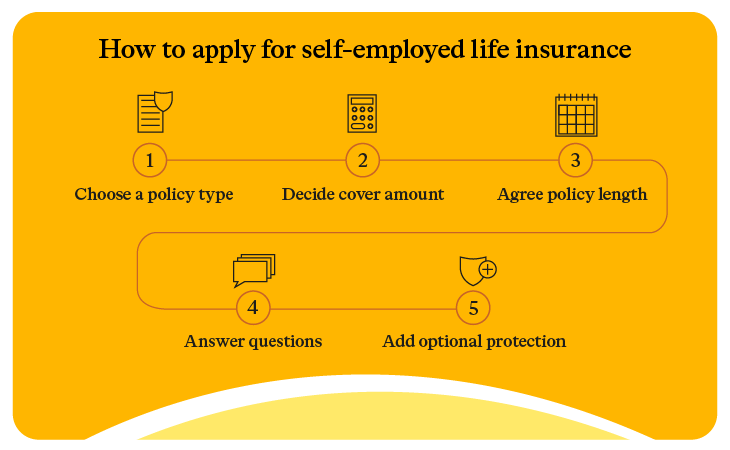

Choosing the right type of policy and applying:

- Choose a type of life insurance. First, you should think about which financial commitments your dependants would need to cover if you were to die. You could get Decreasing Life Insurance, which can be used to protect a repayment mortgage, or Life Insurance which can be used to protect a mortgage or cover a wider range of expenses, including bills and childcare costs.

- Decide your cover amount. This can be based on your self-employed earnings or something else like your mortgage. Choose a life insurance cover amount that reflects how much money your family would need to pay ongoing expenses. You could take your self-employed earnings as a reference point. Our life insurance calculator can help you estimate the amount of cover you might need.

- Agree on the policy length. Depending on your age, your L&G life insurance policy can run for up to 50 years. But you could consider short term life insurance. Decide what's right for you, maybe it needs to last while you’re self-employed or until you’ve repaid a mortgage

- Give honest answers when you apply. An insurer is going to ask questions about you so they can give you a personalised price for your policy. This will include health, lifestyle and your self-employed occupation. Read more about dangerous jobs and life insurance.

- Consider extra protection. Life insurance pays out if you die following a valid claim, but what if you were diagnosed with a critical illness? Critical Illness Cover can be added to Life Insurance or Decreasing Life Insurance for an extra cost.

Making a claim

The claims process is the same for all customers. Including self-employed and permanent employees. An insurer will complete some checks before paying a claim. This could include:

- You're covered by the policy and premiums (the payments you're making for the cover) are up to date.

- You gave honest answers when you applied for cover. It's important to give accurate information about things such as your self-employed occupation. If you don't the insurer might not be able to pay the claim.

- You won’t be covered if within the first year of the policy you die as a result of suicide, intentional and serous self-injury, or an event where in our reasonable opinion, you took your own life.

Read more about how L&G life insurance payouts work.

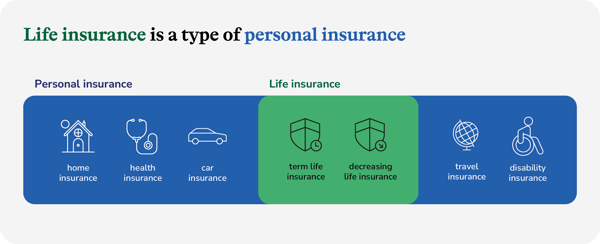

While life insurance can pay a cash sum if you were to die, or be diagnosed with a terminal illness, personal insurance is a broader term that refers to any insurance policy that you take out individually for personal or family protection. So while there is no standalone product called ‘personal insurance’ for self-employed workers, there are various types of insurance which fall under this category.

Types of insurance for the self-employed

When taking the step into freelancing, consulting or contractor work, there are various types of self-employed insurance you may want to consider.

Life insurance

Our Life Insurance could pay out a cash sum if you die or are diagnosed with a terminal illness (with a life expectancy of less than 12 months) while covered by the policy. Given an employer’s death-in-service benefit will only be in place for the duration of your employment, it can be sensible to take out life insurance whether you’re self-employed or not.

Critical Illness Cover

Critical Illness Cover is another form of insurance that can be used for self-employed people, and can be added for an extra cost when you take out Life Insurance or Decreasing Life Insurance. If you work for yourself, critical illness cover is an important option to consider. It could pay out a cash sum if you’re diagnosed with, or undergo a medical procedure, for one of the conditions that we cover during the length of your policy, and you survive 14 days from the diagnosis.

Income Protection Benefit

As you will no longer enjoy the benefit of sick pay if you’re self-employed, what will happen if a long-term illness or injury means you’re unable to work, resulting in a loss of earnings?

With Income Protection Benefit you’ll receive a regular monthly payment if you can’t work due to incapacity caused by an illness, or an injury which results in a loss of earnings. This continues until you return to work, retire, die, or your plan comes to an end – whichever comes first.

Find out more about Income Protection Benefit, which is available through our team of financial advisers.

Reasons to consider ‘self employed life insurance’

Life insurance can be an invaluable form of personal insurance for self-employed people. If you work for yourself, there’s a good chance you’re attracted to the various advantages: choosing when you go on holiday, taking on a variety of projects, and the ability to deduct allowable expenses from your running costs. But compared to a permanent employee, you also don’t receive the following:

- Paid holiday

- Statutory Sick Pay

- Statutory Maternity / Paternity / Adoption Pay

- Statutory Redundancy Pay

- The National Minimum Wage

- Paid time off for emergencies

- Paid compassionate leave.

While being your own boss is appealing, unless you have ‘self-employed life insurance’ such as a term Life Insurance policy, your loved ones will have less protection against the financial impact of your death (or a critical illness if you have Life Insurance and Critical Illness Cover).

If you have a family or dependents who rely on you financially, and if you’ve lost a death-in-service benefit from an employer, life insurance can give added protection and peace of mind if you’re self-employed. Just remember, these are not savings or investment products and have no cash value unless a valid claim is made.

Many self-employed individuals can claim tax deductible expenses, such as travel costs and phone bills, but premiums for personal life insurance are not tax deductible. However, any cash sum payout from a life insurance policy is not subject to Income Tax.

Regardless of whether you’re a permanent employee or self-employed, our life insurance works in the same way for policyholders. Life Insurance can help minimise the financial impact on your loved ones if you die during the length of your policy, helping to reassure you that your family’s way of life is protected should the worst happen.

We also offer a Decreasing Life Insurance policy which is designed specifically to help protect a repayment mortgage, as the amount of cover will reduce roughly in line with the way a repayment mortgage decreases.

Want to learn more about Life Insurance?

Related Articles

Life insurance and tax

Life insurance when moving abroad