Death in service benefit vs life insurance

Death in service is a popular benefit offered by some employers. But who gets death in service benefit and how does it differ to life insurance?

You might also like...

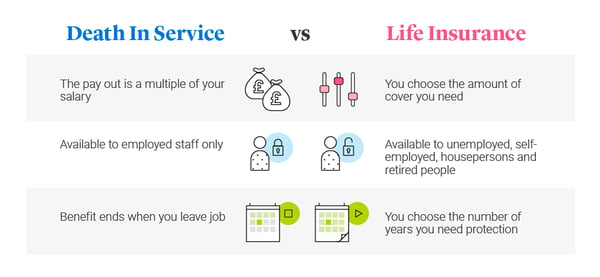

Death in service is an employee benefit. It pays a tax-free cash sum if the employee dies while on the company payroll. The employee can normally choose who receives the money.

If you’ve started a new job and your employer offers death in service, here is what to expect:

- Your employer will tell you if you're entitled to a death in service benefit and when it starts. If you're not sure what you’re entitled to, ask your employer.

- The benefit amount is a multiple of your annual salary. You can name a person who will receive the money if you die e.g. a family member.

- If you die the benefit is payable at the discretion of trustees. If you've asked for a specific person to receive the money, they'll take this into account.

A death‑in‑service benefit is usually paid as a multiple of annual salary. Most UK employers offer between two and four times salary. The Office of National Statistics recently reported average earnings of £38,220 in the UK. Based on that income, a death-in-service payment could be £76,440 at two times salary and £152,880 at four times salary. Some companies may use higher salary multiples to work out death in service payments.

These figures are for illustration only.

No, it is not mandatory for employers to offer death in service benefit. Some employers choose to offer death in service as part of an employee benefits package.

Death in service benefit and life insurance are similar in that both can help protect your loved ones in the event of your death. But that’s where the similarities end.

While it’s easy to confuse the two, death in service is notable for being an employee benefit to help loved ones adjust financially if the employee dies. In contrast, life insurance is a separate policy that you arrange yourself and is designed to pay out a cash sum of your choosing if you die during the length of the policy. A life insurance payout could help pay the mortgage and other living costs, rather than provide compensation with a multiple of your salary.

Death in service benefit payments aren’t usually subject to tax, such as Income Tax or Inheritance Tax. That’s because death in service benefit schemes are normally held in a trust by an employer.

Similarly, if your life insurance is written in trust, the policy is usually exempt from Inheritance Tax.

A Trust is a legal arrangement which allows the owner of a life policy (the settlor) to give their policy to a trusted group of people (the trustees), who look after it. At some time in the future, they pass it on to some people from a group that the settlor has decided (the beneficiaries). The trustees usually have discretion about which of the beneficiaries to pass it on to, how much each will get, and when.

Trustees of a death in service benefit

The benefit may be integral to a pension scheme or provided separately. In almost every case, the arrangements are established under a trust and the trustees have a discretionary power to decide who will receive the lump sum. Usually, the proceeds will be paid to the employee's family.

If approved, a death in service payment would ultimately be paid to your beneficiary. But first, the payment is normally made to the trust established by your employer. The scheme trustees decide who should receive the money.

Trustees typically want to take the employee’s wishes in to account. That's why it's important for you to name the person that you want to receive the benefit, who is sometimes known as your ‘nominated beneficiary’. You can do this by completing an ‘expression of wish’ form provided by your employer.

You will only be covered for death in service if your employer has chosen to offer this benefit. If so, you could receive a lump sum (often between two and four times your annual salary) in the event of your death. Usually, you just have to be on the payroll in order to be eligible, and your death doesn’t have to be work-related. You do not qualify for this cover if you are self-employed.

Bear in mind that death in service covers you as the employee, and not your partner, unlike joint life insurance. This could leave a protection shortfall unless you or your partner have made other arrangements.

If you think you may be eligible, check with your employer so you know what you are entitled to receive.

When an employee leaves an organisation, they will no longer be protected by any death in service benefit. In contrast, you choose the length of a life insurance policy. Providing you keep payments up to date the policy will remain in place until the agreed end date. This is regardless of whether you change jobs or go self-employed.

If you’re covered at work by death in service, here are some of the positives:

- It is normally provided at no cost to the employee.

- The benefit is normally paid tax-free in the event of a claim.

- As long as you’re on the payroll, your death is covered.

- Your loved ones would receive a cash sum – a £25,000 annual salary could trigger up to £100,000 in death in work benefit.

- It's often possible to get death in service cover even if your health makes it difficult to get individual life insurance.

Here are some of the drawbacks compared to life insurance:

- If you change jobs, your new employer may not offer death in service, or the salary multiple could be different.

- If you have previously relied on death in service benefit and need to apply for life insurance at a later date, it could be more expensive as life insurance generally costs more as you get older; or it may also be difficult to obtain cover if your health changes.

- The amount of cover is based on a multiple of your salary, which may or may not be enough to meet your protection needs.

- As it is an occupational benefit, you can only nominate a beneficiary. While it would be unusual for trustees not to pay the benefits as you have asked, this remains a request rather than a binding obligation.

Death in service benefit should be paid quickly once the claim is accepted. The actual time will be affected by the time it takes to provide the provider with the information they need to assess the claim.

A death in service payment isn’t designed to repay a mortgage, although the payment could be used for any purpose. The benefit gives financial assistance to the employee’s family. Your ‘nominated beneficiary’ will decide how it’s spent. It’s worth having a conversation with your loved ones to explain how you would like the money to be used. If you’re thinking about using death in service for mortgage protection, it’s worth considering:

- The benefit could be more or less than the outstanding mortgage.

- You also need to work for an employer that provides this benefit for the length of the mortgage.

- It won’t cover your partner if you have a joint mortgage.

Unlike death in service, life insurance can be tailored to protect your mortgage. If you’re looking for mortgage protection, you can choose level cover that stays the same for the length of the policy. Alternatively you can choose a mortgage life insurance policy, such as Decreasing Life Insurance from Legal & General, where the amount of cover decreases roughly in line with the way a repayment mortgage decreases.

Yes, if you die while contributing to the NHS pension scheme, your nominated beneficiary would be entitled to receive a lump sum. Read the British Medical Association’s online guide to death in service as an NHS employee, GP locum or bank staff.

Death in service is normally paid from a trust directly to your ‘nominated beneficiary’. The benefit does not form part of someone’s estate when this happens. Read our guide on estate planning in later life.

- Check your eligibility. Employers aren’t legally obliged to offer death in service benefit, so it’s worth checking with your HR department to see if you have any protection.

- Estimate your payout. Death in service benefit is usually a multiple of a salary, so you should check how much your loved ones would be due in the event you passed away.

- Assess your spending. Talk to your loved ones about how you would like them to use the benefit. Would your death in service cover meet the cost of expenditure like the mortgage or rent, childcare or household bills?

- Think about the future. No one has a crystal ball, but future decisions – like whether to leave a job, become self-employed or buy a property – could influence the importance you place on death in service benefit.

- Review your life insurance. Once you know how much death in service cover you have, you could assess whether you have sufficient life insurance cover in place. You can sometimes make changes to a life insurance policy if you wish to increase your cover.

What is life insurance and how does it work?

Life insurance is designed to help protect your family financially by paying out a cash sum if you die during the length of the policy. If you change jobs, or even retire, your life insurance will continue until you die or your policy comes to an end. Cover can be arranged on a joint or single life basis to suit your needs.

You can also opt to put your life insurance in Trust so you have peace of mind knowing that the pay-out will go to the people you intend.

Life insurance is not a savings or investment product and has no cash value unless a valid claim is made.

Life Insurance - Your chosen cash sum could be paid out if you die during the length of the policy. It could be used to help protect the family's lifestyle and everyday living expenses or help to pay the mortgage.

Decreasing Life Insurance - Designed to help protect a repayment mortgage so the amount of cover reduces roughly in line with the way a repayment mortgage decreases. This means your loved ones could continue to live in the family home without worrying about the mortgage.

Critical Illness Cover - can be added to life insurance or decreasing life insurance for an extra cost. It pays out if you’re diagnosed with, or undergo a medical procedure for, one of the specified critical illnesses while your covered, and you survive for 14 days from diagnosis. It could help with child care costs, household bills or to help maintain your standard of living if you're forced to take time off work to recover.

Do I need death in service and life insurance?

Having death in service benefit is certainly a positive if your employer offers this perk. But you will want to have a long and hard think about whether a multiple of your salary would be enough to support your beneficiaries or loved ones. For example, if you have an outstanding mortgage balance of £300,000, a death in service benefit of £150,000 won’t cover the ongoing costs.

Death in service might seem attractive if you have no intention of leaving your job. But there is no guarantee you will stay in the same role indefinitely. With life insurance you’ll have the security of knowing how long protection lasts. If you keep paying for your policy, you'll have the peace of mind your loved ones could receive a cash sum.

But of course, having some financial protection is better than no protection. Have a think about the protection you would like and contact us if you have any questions about our life insurance products.

Want to learn more about Life Insurance?

Other related articles

Can you have more than one life insurance policy?

The difference between Critical Illness Cover & Income Protection

10 Myths about life insurance debunked