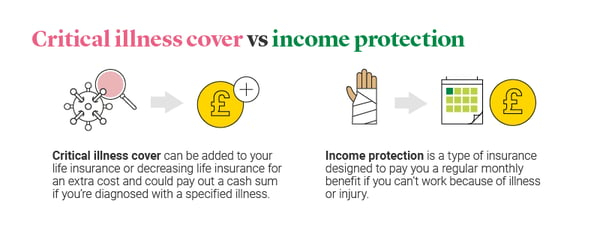

The difference between Critical Illness Cover & Income Protection

Both Income Protection Benefit and Critical Illness Cover are designed to help protect you financially. The difference lies in the fact that Critical Illness Cover is designed to pay out a one off cash sum if a valid claim is made. In contrast, Income Protection Benefit is designed to pay out a monthly benefit if you're off work due to an illness or injury which results in a loss of earnings.

You might also like...

Income Protection

If you’re unable to work due to incapacity caused by illness or injury which results in a loss of income, Income Protection Benefit is designed to pay you a regular monthly benefit until you’re able to return to work or until your plan ends, or you retire, or you pass away, whichever happens first.

As with all insurance policies, limitations and exclusions apply. For example, this plan does not include unemployment cover and will therefore not pay out if you become unemployed. Any monthly benefits should be free from UK Income Tax or National Insurance contributions. The Government may change this tax position at any time, which could affect the monthly benefit your policy pays out. Read more about Income Protection Benefit from Legal & General.

Pros and cons of income protection insurance

In order to compare income protection insurance with alternatives, it’s worth familiarising yourself with the potential advantages and disadvantages of this type of policy.

| Pros | Cons |

|---|---|

| Covers you if you can't work due to incapacity caused by an illness or injury which results in a loss of earnings | Existing medical conditions may be excluded |

| Monthly tax-free payments | Your full income isn’t covered |

| Multiple claims can be made | Can’t be added to your life insurance |

Critical Illness Cover

When you take out life insurance or decreasing life insurance with Legal & General, you have the option to add Critical Illness Cover for an extra cost. It could pay out a cash sum if you’re diagnosed with, or undergo a medical procedure for one of the specified critical illness that we cover during the length of your policy, and you survive for 14 days from diagnosis. Some of the illnesses we cover include:

- Cancer (excluding less advanced cases)

- Heart attacks (of specified severity)

- Stroke (resulting in symptoms lasting at least 24 hours)

For full definitions and when you can claim for these illnesses please refer to our Guide to Critical Illness Cover PDF and Policy Terms & Conditions PDF.

Please note that some types of cancer are not included and you need to have permanent symptoms to make a claim for some illnesses. This is not a savings or investment product and has no cash value unless a valid claim is made. Read more about the critical illnesses we cover

Pros and cons of Critical Illness Cover

If you’re not sure about how Critical Illness and Income Protection compare, the below may shed some light. We explain why you may (and may not) want to protect yourself with Critical Illness Cover.

| Pros | Cons |

|---|---|

| Choose how much cover to take out when you apply | Not all illnesses are covered |

| The cash sum can pay for childcare costs, household bills and everyday living | Doesn’t cover minor injuries |

| Covers many types of cancer, heart disease and strokes | Your insurer ultimately decides if your diagnosis matches its definition |

| You may be able to increase your cover without a medical | You can’t make a claim until 14 days after your diagnosis. |

| Includes Children’s Critical Illness Cover | Your cover ends when a payout is made under full cover. |

You can hear more about Critical Illness Cover from our expert Barry, in this short video.

22 Dec 2025 / 01:34

Let's compare income protection vs critical cover

Critical Illness Cover and Income Protection Benefit are designed to meet different needs, so naturally, there are differences between these insurance products. Here, we compare these types of insurance at a glance:

| Income Protection Benefit | Critical Illness Cover |

|---|---|

| Designed to pay out if unable to work due to illness or injury | Pays out if you’re diagnosed with a specified illness |

| No lump sum | Pays a lump sum |

| Pays a monthly benefit for a valid claim | Pays out once (for a valid claim) |

| Pays out after a waiting period of 4, 8, 13, 26 or 52 weeks – it's up to you. Pay outs are monthly in arrears | A claim can be made if you survive for 14 days from diagnosis |

Related Articles

Life insurance with pre-existing medical conditions

Life insurance

Types of life insurance

What is the difference between health insurance and life insurance?