Life insurance with pre-existing medical conditions

For the purposes of your life insurance cover, a pre-existing medical condition is any illness or injury that exists before, or at the time you take out a life insurance policy.

Examples of pre-existing medical conditions and events include, but are not limited to, the following:

Diabetes

Heart conditions (including angina, heart attacks and heart valve problems)

A stroke (including mini strokes) and brain haemorrhage

Cancer

Epilepsy

Mental illness

Neurological disorders such as multiple sclerosis

Kidney illnesses

Asthma and breathing problems.

High BMI

You may want to explore the options below.

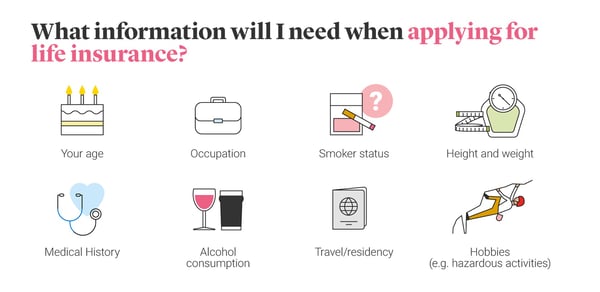

You don’t always need a medical exam when applying for life insurance. We’ll decide whether an exam is required based on the amount of cover applied for and your answers to the application questions. We will want to know the following information about you:

- Your age

- Occupation

- Smoker status

- Height and weight

- Medical history

- Alcohol consumption

- Travel / residency

- Hobbies (such as hazardous activities)

If you’re in good health, then it’s likely you’ll be offered life insurance on standard terms without a medical exam. In some cases, we may ask you to complete a medical exam before we can offer you a policy.

No – L&G will pay for the costs of any medical exam we request after receiving your life insurance application.

A life insurance medical exam could be with a doctor or a nurse and we might arrange for this to happen in your home or near your workplace. Every application is different, and we may require a short health check, and/or discuss your medical history. Examples of what may happen in a life insurance medical check-up include:

- Weight and height measurements to determine your Body Mass Index (BMI)

- Waist measurement

- Blood pressure and pulse checks

- Urine testing for blood, glucose and protein

Life insurance medical testing

If you are asked for additional testing during your exam, this could include any of the following:

- A test to confirm your smoking status (if you have told us you are a non-smoker)

- Human Immunodeficiency Virus (HIV) test – When applying for life insurance, HIV tests are commonplace, especially for higher cover amounts

- Other tests for life insurance can include blood tests and/or an electrocardiogram.

But before any medical testing or exams for life insurance take place, you’ll need to tell us about your medical history and any pre-existing conditions you have.

Why you’ll need to tell us about any pre-existing conditions

How much you pay for life insurance (your premium) can be affected by existing conditions if your application is accepted. Sure, it’s easy to see why some people would be half-tempted to avoid mentioning their medical history in order to get the cheapest cover. But in reality, if you do not tell us full and accurate information about your health when applying then any future claim may not be paid, leaving your loved ones without the cover that you thought your life insurance policy would provide.

There are a lot of medical conditions that will still allow you to get life insurance. But every individual is different, so to find out if you're eligible for cover it may be best to speak to an adviser or your preferred insurance provider for some guidance.

Critical Illness Cover can be added when taking out Life Insurance or Decreasing Life Insurance policy for an extra cost, and is designed to pay a cash sum if you’re diagnosed with a specified critical illness during your policy term and you survive for 14 days from diagnosis.

Some pre-existing conditions would mean we would be unable to offer Critical Illness, where others may mean we charge an extra premium or exclude the specific condition from the cover. However, every applicant is assessed on an individual basis, and even if you were unable to get cover for a particular condition, there are many illnesses covered by Critical Illness Cover in certain circumstances – including many types of cancer, heart attack and stroke.

Read our guide to Critical Illness Cover with pre-existing conditions.

In order to work out your premiums and decide if cover can be offered with a particular pre-existing condition, or without the need for a medical exam, simply complete a life insurance application and answer the medical questions you’re asked. If you give details of a health condition, you may need to provide more information such as:

- The name of the condition you have

- The date you were diagnosed

- Details about any hospital admissions and any specialist referrals

- The severity and regularity of your symptoms

- Information on how it affects your everyday life, such as absences from work

- Any medication you take as well as the date you started.

Sometimes a medical report from your doctor may be required. Remember, your insurance company needs your consent before they can request a medical report from your doctor. If a medical report is requested, you will be notified, and will have 21 days to arrange a consultation with your doctor to review it, if you wish.

As long as you supply full and accurate information in your original application, and pay your premiums when due, your life insurance cover will remain in force for the duration of your policy. If you’ve provided inaccurate information, an insurer has the right to invalidate your policy.

You’ll be asked about any family illnesses when you make your life insurance application. Your acceptance terms may be affected by the nature of the condition.

Related articles

How are life insurance premiums calculated?

What critical illnesses are covered?

How much Critical Illness Cover do I need?

Get the most out of an online doctor’s appointment

Coping with terminal illness

Will my family medical history affect my life insurance?

Can you get life insurance with no medical?