Life insurance and cancer

One in two people in the UK will at some stage develop a form of cancer, and of course the consequences can be tragic for families. But how can life insurance provide financial protection after a cancer diagnosis.

Life insurance and cancer explained

All thing’s considered, it’s little wonder why so many people wish to take out financial protection against the impact cancer would have. Life insurance can be part of that planning.

Life insurance pays out a cash sum if you pass away, or if you’re diagnosed with a terminal illness during the length of your policy. So, if cancer is the cause of death or is the cause of a terminal illness diagnosis then, yes, it is covered.

With L&G, a terminal illness is defined as having a definite diagnosis by your hospital consultant of an illness that satisfies both of the following:

- The illness either has no known cure or has progressed to the point where it cannot be cured; and

- In the opinion of your hospital consultant and our Medical Officer (a qualified doctor employed by L&G), the illness is expected to lead to death within 12 months.

Additionally, if you add Critical Illness Cover for an extra cost when taking out a life cover policy with us, you’ll have further financial protection in the event you’re diagnosed with a specified condition or undergo a medical procedure covered by the policy. In order to claim for cancer (excluding less advanced cases), your diagnosis would need to meet the definition in the Policy Terms and Conditions.

But what are your life insurance options if you already have cancer, or a history of cancer? Learn more.

There are around 200 types of cancer, many of which are covered by L&G’s Critical Illness Cover. But what matters isn’t just the type of cancer but the extent to which the cancer has spread, and where it originated.

Some types of cancer are not covered by our Critical Illness Cover. For example, we do not currently cover cancers that are ‘historically classified’ as pre-malignant or non-invasive. The ‘historical classification’ refers to the type of tissue and location of the body where the cancer started.

You can find more information about the conditions covered in our Policy Terms and Conditions. If you already have Critical Illness Cover with us, please refer to your original policy documents for the full terms and conditions and definitions available to you, as the conditions you’re covered for may be different.

Does Critical Illness cover skin cancer?

Some skin cancers are covered by L&G Critical Illness Cover, but it depends on how localised the spread is. Malignant melanoma, for example, is not covered unless it has been ‘histologically classified’ (referring to the scientific study of tissues) as having caused invasion beyond the outer layer of skin, or epidermis. Similarly, Critical Illness Cover can include other skin cancers, when it has been classified as having spread to distant organs or caused invasion in the lymph glands.

Does life insurance cover prostate cancer?

Life Insurance with Critical Illness Cover includes prostate cancer tumours in cases where the tumour has been classified with a Gleason score of 7 or above – this is the most frequently used grading system for prostate cancer. You can find out more in our Guide to Critical Illness Cover (PDF).

Is thyroid cancer covered by critical illness insurance?

It’s possible to make a successful claim on a critical illness insurance policy following a thyroid cancer diagnosis. But it's always important to remember that each claim is looked at individually and other factors may be in taken in to account. For example, L&G do not currently cover cancers that are ‘historically classified’ as pre-malignant or non-invasive.

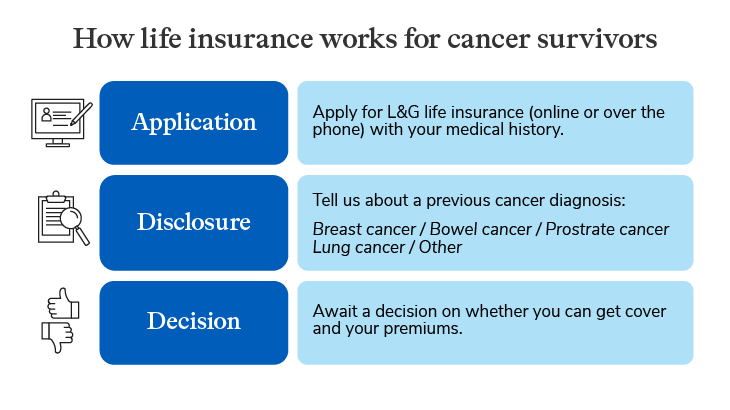

Yes – depending on the nature and extent of the cancer, it’s possible to get life insurance after surviving certain cancers. This includes the four most common types of cancer:

- Breast cancer

- Bowel cancer

- Prostate cancer

- Lung cancer.

Life insurance after cancer – how it works

In theory, you can get L&G life insurance after a cancer diagnosis, but your application will be assessed individually.

If you’ve previously had a cancer – such as breast, bowel, prostate or lung cancer – there may be a period of time before you can get life insurance. Additionally, the amount you pay for the policy (the premium) may end up higher.

You will need to tell us about your medical history when you apply for cover. The decision regarding your application won’t just be on the basis of your cancer history; it will also take account of things like your age, other medical information, and how much cover you wish to take out.

Can I get life insurance after cancer if I’ve been in remission?

There isn’t a fixed remission period if you’re applying for L&G life insurance after cancer, but if you have been without cancer symptoms for an extended period of time, you could potentially be offered life insurance at standard rates. But remember, your age – and other factors – will also influence the outcome of your life insurance application.

Can I get critical illness life insurance after cancer?

Yes, you can get critical illness cover after cancer, but whether you get cover depends on factors like the type of cancer and its severity. Read more about some of the critical illnesses we cover.

If you are aged 50-80 and have cancer - or a history of cancer, there is also the option of Over 50 Life Insurance, which has guaranteed acceptance with no medical questions.

The maximum amount of cover is £10,000, so whether Over 50 Life Insurance would be suitable depends on your needs. Nevertheless, this type of life isnurance could be an affordable way for you to leave some money for your loved ones after you die. It could be used to help settle unpaid bills, put towards a small gift, or to help towards the cost of a funeral. Full cover is payable after one year.

Other types of life insurance may be available if you can answer health and lifestyle questions. Speak to an adviser if you need help.

A family history of cancer can affect both a life insurance and critical illness cover application. For example, inherited conditions, like certain types of bowel, breast or ovarian cancers could make cover more expensive. For Critical Illness Cover we might not pay a claim that’s linked to your family history.

We’ll always explain what your policy will cover and how much it will cost before you buy. That means you can make an informed decision about whether to go ahead or shop around.

Resources for those affected by cancer

We understand that getting a cancer diagnosis is a difficult time for anyone. For our part, we want to ensure that if you have an existing policy with us, the process of making a claim should be as straightforward as possible. Please see your policy documents for more information

Here are some resources with more information about cancer and life insurance, as well as cancer in general.

Want to learn more about Life Insurance?

Related articles

Coping with terminal illness

Is Critical Illness Cover worth it?

Life insurance with pre-existing medical conditions

Types of life insurance

High Risk Life Insurance