What happens to someone's debts when they die

When someone dies, their estate is responsible for any debts. This means that any outstanding debts will usually be repaid using money or property remaining in the estate.

You may also be interested in...

Debt after death: the key points

Dealing with the debts of a deceased person presents a challenge for any family or individual. Below, you can find key information and learn more about what happens to debt after someone had died:

- What happens to debts when someone dies?

- Are families responsible for debt after death?

- Do credit card debts die with you?

- Sorting out the debts of someone who has died

- How to deal with debts as the executor

- Dealing with debt if there is no insurance

- Joint debts

- Undisclosed debts

- Secured and unsecured debts

- What to do if there’s not enough money

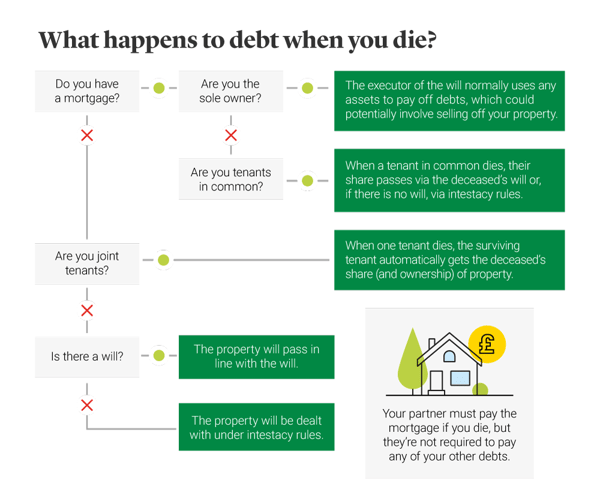

- There is a will. The deceased chooses someone they trust to manage their estate. This is often an immediate family member or spouse. The Personal Representative is executor of the will.

- There is no will. In the absence of a will, the court appoints someone to represent the deceased. The Personal Representative is the administrator of the estate.

A Personal Representative repays debt from assets in the deceased's estate. They are not personally liable for the debts of the deceased.

Where we have explained an executor has to take an action, it also applies to an administrator.

Following a death, the executor of the estate is the person(s) responsible for dealing with the will and estate. They will need to apply for a Grant of Probate which allows you to legally manage the deceased person's assets. If there's not a will you have to apply for a Letters of Administration to do so.

As the executor or administrator, you can use any remaining assets from the estate to pay off the debts. You are also liable to pay Inheritance Tax on property that forms part of the deceased’s estate.

Later, we explore what happens to debt when there is no money in an estate after someone dies.

Debt isn’t inherited in the UK, which means that family, friends or anyone else cannot become responsible for the individual debts of the deceased.

You’re only responsible for the deceased person’s debts if you had a joint loan or agreement or provided a loan guarantee. So in short – you aren’t automatically responsible for a spouse’s or registered civil partner’s debts. Those debts are likely to have to be paid from the estate of the deceased.

A common misconception is that any credit card debts are automatically written off. Instead, any individual debts must be paid using the money the deceased has left behind. Only if there isn't enough money in the estate may the debt be written off.

A personal credit card with an outstanding unpaid balance is an example of individual debt.

Sorting out the debts of someone who has died

In the aftermath of a death, it can of course be difficult to move on to practical tasks. So when it comes to dealing with a deceased person’s debts, it can be useful to have a priority order. Once you’ve received a Grant of Probate or Letters of Administration, here are some first steps you could take:

How to deal with debts as the executor

As the executor of the estate, here are some practical steps you can take – and issues to consider – to make sure the deceased’s debts are taken care of.

- Contact creditors and explain the situation, asking them to send a statement outlining anything still owed.

- Make sure that in the case of an individual debt, like a credit card debt, the bank immediately stops taking any scheduled Direct Debits from the deceased’s bank account.

- Note that in the case of a joint bank account, the surviving partner becomes the sole owner of the account, and remains responsible for any debts.

- If it is a joint debt, then the name of the deceased can be removed from the debt.

- With any luck, the deceased will have put all the relevant documents together – including insurance policies – and will have let someone know where they are, or even included such details in their estate plan.

- Remember to check paper records, computers, memory sticks, and cloud-based storage for digital versions of documents.

Dealing with debt if there is no insurance

If there is no insurance in place, what happens to debt when someone dies? The executor of the will should contact the creditors to make arrangements to pay off the debts, assuming they haven’t already made a claim on the estate.

If there is no life policy to cover the mortgage, and the beneficiaries named in the will – or under the rules of intestacy – have no wish to obtain, or do not qualify for, a mortgage, then the property may be sold to cover the outstanding debt.

Types of debt when someone has died

Once the Personal Representative of the will has probate, or grant of administration, the money from the deceased’s estate can be used to pay off any outstanding debts. But first, you’ll want to understand what types of debt you’re dealing with.

How to pay off someone's secured and unsecured debts

If someone has passed away and you’ve been tasked with managing the estate, there are different ways you might tackle each secured or unsecured debt.

Mortgages

When it comes to the deceased’s mortgage, the lender still has the right to demand that the mortgage is repaid in full. So as the executor, here are three steps you could follow:

- Find out if the deceased had a life insurance policy. If they do you could make a claim in order to pay off some or all of the mortgage.

- If there is no life insurance, decide whether you want to keep the property and take on the mortgage. You (and anyone else named in the will) have the right to transfer ownership to yourself.

- Alternatively, you can sell the property – known as a ‘probate sale’ – and use the proceeds to repay the lender. You will need to pay any Inheritance Tax due within six months.

Cars

Similarly, if the deceased has an unsecured car loan debt, you may decide to sell their vehicle in order to settle the outstanding balance. If the debt is secured, the car finance company may choose to auction the vehicle and claim any outstanding funds from the estate. You will also need to inform the DVLA when the registered car owner has died.

Loans

For unsecured debts like personal loans and credit card debts, here are some steps you can follow.

- Locate the original signed loan agreement to see if anyone other than the deceased is listed.

- Contact the deceased’s bank to settle the outstanding debts using money from the estate.

- Confirm that the payment has been processed so the bank can update its records.

It’s worth remembering that only the person who signed the credit agreement can be held personally liable for credit card debts, though the money will still need to be repaid by their estate.

Bills

As the executor you will be responsible for settling the deceased’s final utility bills such as water, gas and electricity. Here is how you can repay these debts.

- Inform each utilities company that the account holder is deceased and that you will be paying off the outstanding balance.

- Provide them with any required information, such as the most recent meter reading.

- Pay the final bill using money from the estate and ensure any Direct Debits are cancelled.

If there are insufficient funds in the estate to pay off the deceased’s debts, as well as funeral costs and other expenses, this is known as an insolvent estate. If that applies, there is an order of priority as to how the debts are paid. The payment of debts must be completed before the estate can be divided between heirs.

Here are some useful tips, resources and steps you can take to settle the outstanding debts in this scenario.

-

Decide on the order in which lenders should be repaid. For example, you could prioritise the largest lender first.

-

Speak to family members to ascertain whether the deceased had any assets you were unaware of, such as cars or jewellery, which could be sold to raise funds.

-

Check whether they’re due any tax refunds – for example, contact the DVLA to assess their vehicle tax status.

-

If you’re waiting to sell a probate property, you could decide to repay the Inheritance Tax from your own funds if you wish to avoid a fine. You could then recover the money when a property has been sold.

-

Contact the Law Society if you wish to hire a solicitor to offer independent legal advice.

-

Explore some of the resources on GOV.UK for managing debt, such as the Citizens Advice Service.

Writing your policy under trust is a legal arrangement which allows the owner of a life policy (the settlor) to give their policy to a trusted group of people (the trustees), who look after it. At some time in the future, they pass it on to nominated people from a group (the beneficiaries) as chosen by the settlor. The trustees have discretion about which of the beneficiaries to pass it on to, how much each will get, and when.

Placing your policy under trust ensures a quicker payment, without the need for probate, and as the policy falls outside your estate it could help reduce your Inheritance Tax liability (IHT).

Find out more about our life insurance

More articles and guides

What are the duties of the executor of a will?

What happens if you die without a will?

How much can I gift to my grandchildren?

The importance of writing a will