Find out how life insurance can help protect your loved ones.

What happens if you die without a will?

Understandably, no one likes to talk about death. But dying intestate in the UK is something that can be avoided. But what do we mean by ‘intestate’, and what happens to bank accounts and life insurance when someone dies without a will? In this guide we’ll take a closer look at intestacy rules in the UK.

Reviewed by Thomas May

Dying without a will

If you die without writing a will in England and Wales, your property and money will be shared out according to a legal default, rather than your own expressed wishes. Dying without a will is known as dying ‘intestate’, a word with Latin origins which essentially means ‘without a testament’. It doesn’t matter how close you are to certain relatives; if no will is made before you die, your assets and money will be allocated according to the same intestacy rules as anyone else.

In England and Wales, the intestacy rules are set out in the Inheritance and Trustees’ Power Act (2014), which has different implications depending on your circumstances:

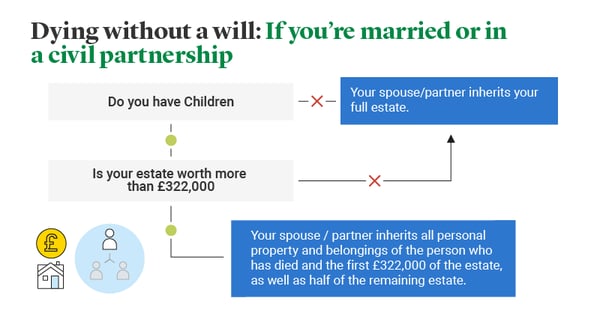

In essence, the husband, wife or civil partner keeps all the assets (including property), up to a value of £322,000, and all the personal possessions, regardless of their value. The remainder of the estate will be shared as follows:

- The husband, wife or civil partner gets an ‘absolute interest’ (full rights) over half the remainder.

- The other half is then divided equally between the surviving children.

If a son or daughter (or other child where the deceased had a parental role) has already died, their children will inherit in their place.

Here are some other permutations:

- If you’re married or in a civil partnership but have no children, your surviving spouse will receive everything in the estate.

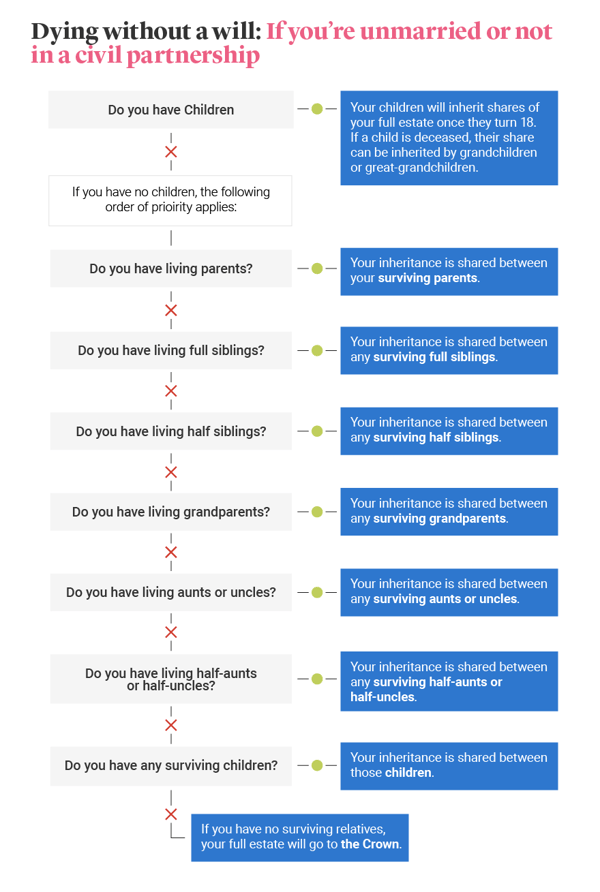

- If you’re unmarried and have children, they will inherit the entire estate on their 18th birthday, with equal shares if there is more than one child. Grandchildren or great-grandchildren can inherit the share if the children are deceased.

- If you’re unmarried with no children, your estate will be allocated in the following order: your parents, full siblings, half-siblings, grandparents, uncles and aunts (then their children), half-uncles and half-aunts (then their children).

- If you’re unmarried and have no living relatives, all your money and assets will go to the crown.

There is no one-size-fits all for dying without a will in the UK, as intestacy rules differ in Scotland, where a surviving spouse or partner can claim ‘prior rights’ to a share of property and assets. You can find out what dying without a will would mean for you on the UK government website.

It’s important to remember that in the UK, cohabiting couples do not have an automatic right to make a claim on their deceased partner’s estate. They may be able to make a financial claim if they can prove they were financially dependent on the deceased.

How to find out if someone has left a valid UK will

Ideally, anyone who has written a will should inform all named executors in advance, and make sure they know where the will is kept, which could be a place of residence, a solicitors’ office or a bank, for example. But if someone has recently died and you want to search for a record of the will, you can find a will online through the Probate Service. A small fee is charged for each copy of a probate record.

If you’re a named executor in the will, you’ll need to apply for probate, which gives you the legal authorisation to deal with someone’s property, money and possessions. The process should be straightforward if you’re a surviving spouse – in fact, you wouldn't need a grant of probate if you and your married partner owned assets jointly – but it may take longer for siblings.

If you’re still unable to locate the will but you know it exists, you can report that the will is lost as part of your probate application.

What happens when a will is invalid?

For a will be to valid in England and Wales, it must be witnessed in the presence of two adults 18 and over. Also, they must not be potential beneficiaries of the will, which may includes spouses, civil registered partners of beneficiaries, or members of your own family. If your will is not witnessed or written properly, you run the risk of having an invalid will.

The legal requirements for creating a valid Will in Scotland is only one witness is required, but the Granter (individual making the will) must sign every page of the Will to ensure its validity. The witnessed in Scotland means anyone who is 16 years and over.

If you’re married or in a civil partnership and have followed the correct legal procedures, you’re unlikely to have to worry about contesting an invalid will. But problems can arise in situations where the deceased person is not married or in a civil partnership; for example, unmarried, cohabiting couples with children from previous relationships have the least protection when a will is declared invalid. In this scenario, intestacy rules would apply, and the deceased’s children and relatives would automatically have a claim to an inheritance, rather than a surviving partner.

What happens to a bank account when someone dies without a will?

When a person dies having written a will, their bank debts become the responsibility of their estate, and the named executors must repay any debts with the deceased’s assets. But when there is no will, the process is more complicated. You can still apply for probate, but it is known as a grant of ‘letters of administration’, which gives you the legal right to administer the estate, including access to bank accounts. You will need to value the deceased’s assets, including investments, pensions and life insurance, and provide certified documentation when you apply for probate. It’s recommended that you contact a probate solicitor or accountant in order to ensure the deceased’s money and assets are administered properly according to UK intestacy rules.

Who is my next of kin?

Next of kin is best described as your closest living relative, such as your spouse or civil partner. This is not a term that is legally recognised in the UK. However, there are specific rules as to who takes responsibility when someone dies – usually this refers to loved ones in the following order of priority:

- A spouse or civil partner – It is important to remember that even if you are in a long-term relationship with your cohabiting partner (England and Wales) they are not automatically entitled to an inheritance if you aren’t married or in a civil partnership.

- Children – if they’re 18 or over, your children may be considered next of kin if there is no surviving spouse or civil

- Parents – your parents would be viewed as your next of kin if you have no spouse or civil partner, or any children, or if your children are under the age of 18.

Note: the law does not distinguish between children ‘born out of wedlock' or otherwise in terms of making an inheritance claim. However, if your parent does not appear on your birth certificate, it may be harder to make an inheritance claim without doing a DNA test to give evidence of your parentage.

Protect your family’s future

Of course, there is more to life than money. But writing a will means you can support those who depend on you financially, such as your spouse, children, or a cohabiting partner and make sure there's one less thing they need to take care of in the event of your death. It also gives you the chance to leave a legacy to friends or charities close to your heart. Making a will may also help reduce the amount of Inheritance Tax that might be payable on the value of the assets and property you leave behind. When you consider all this, dying without a will is best avoided.

Find out more about writing a will to ensure peace of mind for you and your loved ones.

Find out more about our life insurance

Related articles

The importance of writing a will

Writing a will is important in making sure your loved ones inherit your money and assets after you’re gone. But what should you put in a will? Read our guide.

Making a will online

Online will writing services make it easier to protect your loved ones after you've gone. Find out more and make a will online.

Over 50s life insurance vs funeral plans

What are the advantages of over 50s life insurance versus funeral plans? Read our verdict and decide how to cover the cost of your funeral.

Can a will be changed after death?

A beneficiary can change a will after death by organising what’s known as a deed of variation. But what is a deed of variation? Find out in our guide.

What are the duties of the executor of a will?

The executor for a will has a range of responsibilities following the death of a friend or family member. Learn more in our L&G guide.