Financial considerations for the bereaved

In the aftermath of losing a partner, it can be overwhelming to think about life after their passing. Coping independently doesn’t mean facing these tasks alone. There is plenty of help available when you are ready to deal with financial matters. This guide aims to help you navigate handling bills, bank accounts and debts as well as explaining the financial support for bereaved families that may be available.

Managing the finances after your partner dies

Taking care of arrangements, digital legacy and other things that need to be done when someone dies is exhausting when you are grieving. It’s important to lean on emotional support like friends and family during this time. Particularly when new financial responsibilities require your attention

Taking over the bills

If you plan to continue living in the same household, this is your top priority to avoid incurring unnecessary late payment fees:

- Make a spreadsheet or write a list of all the bills in one place, recording the dates for when each bill is paid and how much.

- Check whether you can cover the overall amount.

- Start contacting utility bill providers to change the account holder’s name to yours.

Changing payment details

Banks need to be informed when somebody has died, even if you intend to keep your joint account. You may need to think about the following when it comes to paying bills:

- Joint account – Bills can keep coming out of here if you decide to keep the account.

- Personal account – When the bank learns of your partner’s death, their account is likely to be frozen. It is important to switch utility bill debit details to your bank account.

To save you having the same conversations with different banks, the Death Notification Service is a free, online service which allows you to notify a number of organisations of your partner’s death at the same time.

Dealing with debt

Debt includes outstanding balances in their name for credit cards, store cards or hire purchase agreements and debts that you jointly owe, like mortgages. Gather a full list of debts together and find out how much is left on each. Prioritise which need dealing with first – generally, secured debts against an asset/property i.e., mortgage should be paid first, followed by priority debts like Council Tax, then unsecured debts like utility bills or credit cards.

What happens to your partner’s debts when they die?

They become a liability on their estate, which means that they will be paid from money or property left behind. However, it can be more complicated if someone dies without a will.

As a spouse, civil partner or cohabiting partner of the deceased, you won’t usually be responsible for covering debt, unless you are a guarantor or co-signatory of the debt. If there isn’t enough money or assets to pay, the debts are paid in priority order, then written off. Joint debt (where two or more people taken out a loan) is usually passed on to the other person/people.

How to pay off your partner’s debt

- Let creditors know that your partner has died and that you are going through the legal process of dealing with their estate. You will need a statement of the outstanding balance.

- Check whether your partner has insurance, for example life insurance to pay off the debt in case of death. If yes, double check the terms. If not, then you will need to make arrangements for affordable payments if a claim hasn’t been made on the estate. Learn how life insurance payouts work.

- Using your partner’s assets, pay debts off ensuring funeral expenses and administration of the estate are covered first.

Taking over the mortgage

Firstly, speak to the lender and tell them that your partner has died. A mortgage is usually the first debt paid out of the estate or from life insurance. A new mortgage application in your name will need to be made for any remaining debt left on the house after an insurance claim.

Find out more about what happens to debt when you die.

Taking over insurance

Most policies terminate when the main policy holder dies, but this could leave you unprotected. You’ll need to amend the following

- Car insurance - if you’re a named driver, check with the provider to see if you are still insured. Otherwise, you will need to start a new policy.

- Home insurance –a change to the amount of your mortgage can affect your cover and the price. Shop around for a new deal that best suits your new situation.

- Life and protection insurance - if your partner was the person insured, ask the provider if you can make a claim. If it's your policy, think about who should benefit instead of the deceased.

Financial support for bereaved families

If you have lost your spouse or civil partner, regardless of income, you may be entitled to bereavement benefits from the government.

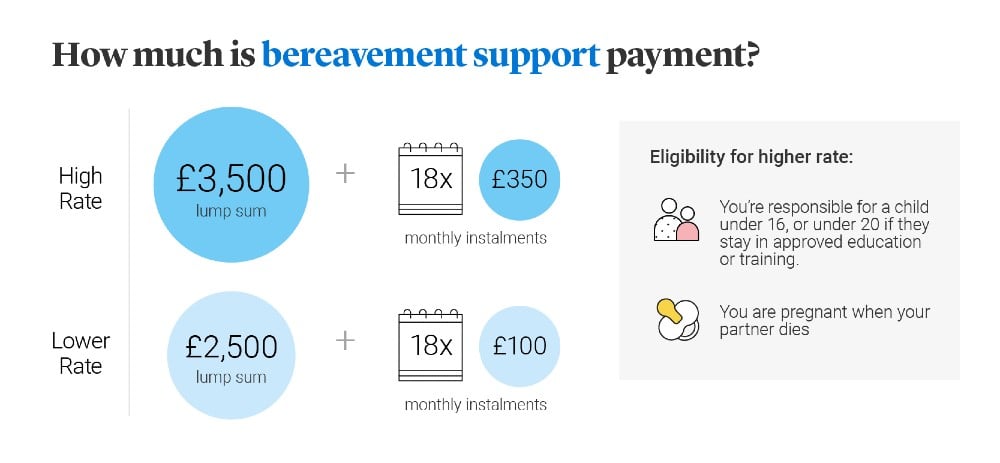

What is Bereavement Support Payment (BSP)?

This is a tax-free lump sum payment initially, followed by monthly instalments for up to 18 months for anyone who has lost a husband, wife, or civil partner.

Who is eligible to receive Bereavement Support Payment?

Who qualifies for bereavement benefit is very straightforward. If your husband, wife, or civil partner died on or after 6th April 2017, you may be able to claim. It could be available if you were living with the deceased as if you were married.

There are two rates of Bereavement Support Payment. If you are eligible for Child Benefit (you don’t have to be claiming this to qualify), then you may receive the higher rate of a £3,500 initial lump sum, followed by 18 monthly instalments of £350.

If you were pregnant when your partner died, you may also receive this rate. The lower rate applies to everyone else and consists of £2,500 for the first payment, and a further £100 per month for 18 months. Making a claim within 3 months of your partner’s death may entitle you to the full amount.

If you receive other benefits, the Bereavement Support Payment won’t affect them for a year after the first payment, but after this time it might affect other government benefits you renew or make a claim for.

Planning for the future

Once you have a handle on the new household finances and you’re feeling ready to look ahead, it’s a good idea to budget and plan for the future. Immediate savings you can make may include a reduction in Council Tax if you now live alone and getting cheaper tariffs on energy bills.

Make a list of all of your household outgoings against all regular income, benefits and savings. This will help you make manage your finances going forward.

Related articles

Coping with terminal illness

What’s the difference between critical illness and terminal illness?

Do I need life insurance?