What is common law marriage?

It’s a common misunderstanding that after living together for a number of years, sharing children or a getting mortgage together, a couple are considered to be partners in a common law marriage. But what does common law partner mean exactly? And what rights do common law partners have?

According to the UK Parliament, “the number of couples choosing to live together (cohabit) without getting married or entering a civil partnership, in what is often called “a common law marriage”, increased by 144% between 1996 and 2021.”

Many cohabiting couples believe that this idea of common law marriage means they will automatically receive the same legal rights as those who are married or in civil partnerships. Instead of being a husband, wife or spouse, they would be known as a common law partner or spouse.

You might also be interested in...

Currently in the UK, common law marriage doesn’t have legal recognition. It's a common myth that once a couple has cohabited for over two years, they automatically have financial protection as a married couple and too many people find themselves in unexpected financial situations after a relationship breaks down, or they suffer the loss of a partner and they need to consider financial matters.

But that’s not to say that your only right to financial protection is via a wedding or civil ceremony – there are still ways you can protect your family’s finances.

What are the implications of common law marriage for couples?

Unlike marriage or civil partnerships, common law marriage doesn't have legal status. There are limited rights available to cohabiting partners in some situations, as we’ll explore below.

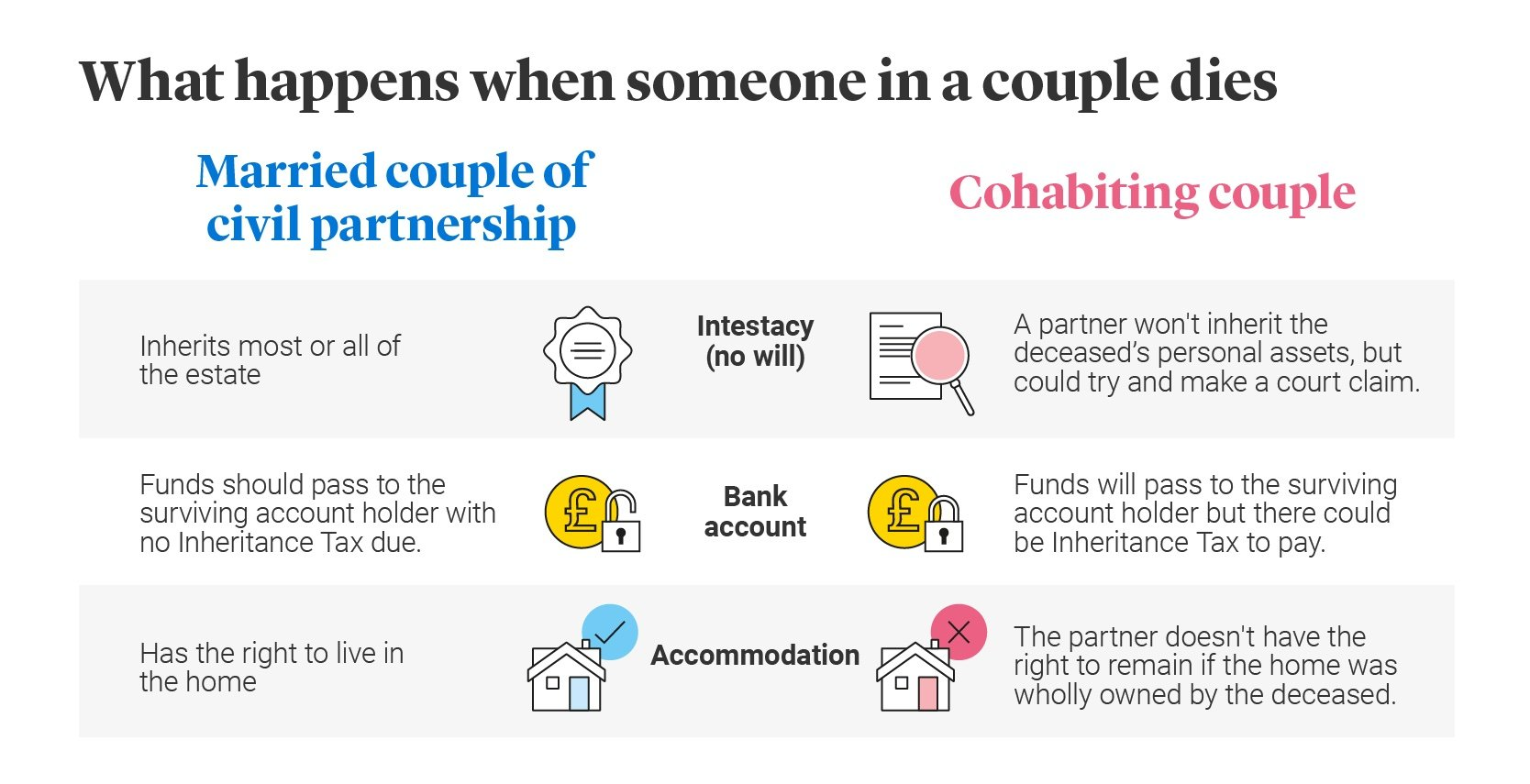

There is no legal right for cohabiting partners to inherit their couple’s estate. This is regardless of whether they have children or the length of time they’ve been in a common law marriage. A surviving partner may be able to legally claim “reasonable provision for their own maintenance”. In other words, financial assistance, if they haven’t been factored into the deceased’s will.

If a relationship breaks down, cohabiting couples have no automatic legal rights to each other’s property. If there is a dispute, a judge may consider the evidence supporting each persons claim. This includes who is the named legal owner and whether a cohabitation agreement covers ownership.

As a cohabiting partner, you’re not entitled to any of your partners state pension. When it comes to your partners occupational pension, you don’t have a right to claim on separation. However, a common law partner can choose who will receive the pension pot if they die before it’s used. It's also possible for the pension holder to arrange a ‘survivor pension’ for an unmarried partner who is financially dependent.

Mothers automatically have parental responsibility for a child at birth. Unmarried fathers don't have automatic parental responsibility. They would need to put their name on the birth certificate, with the mother's consent.

Cohabitating couples are considered “unconnected individuals” by HMRC. They are unable to claim certain forms of tax relief and entitlements, such as Marriage Allowance.

Means-tested benefits, such as Universal Credit, are claimed on behalf of the ‘family’. This means it’s possible for cohabiting couples to get certain financial assistance from the government. Cohabiting individuals can claim bereavement benefits if they have dependent children.

What can cohabiting couples do to protect themselves?

Marriage and civil partnerships confers legal and other rights. That’s not to say that your only right to financial protection is via a wedding or civil ceremony. Below are some ways you can protect your family’s finances.

1. Take out a cohabitation agreement

A cohabitation agreement is a great way for couples to safeguard their joint finances when they live together. It is a legal document detailing what each partner is entitled to if the relationship breaks down. You can easily find a template online to help you create one at home, but it’s best to seek legal advice before signing anything.

2. Write a will

It might not be the cheeriest activity, but it is a great way to make sure your partner is considered within the inheritance you leave. This is important, as if you aren’t married and one of you passes away, the other is not automatically entitled to your property or assets left behind.

3. Nominate a beneficiary for your workplace pension savings

Unlike a state pension, you can tell a workplace pension provider who you would like to benefit if you were to die before you can access your pension savings. Bear in mind your nomination won’t be legally binding, but it would be taken into account by the pension scheme administrator.

4. Asserting property rights

If you buy a property as a cohabiting couple, you can set out your joint ownership arrangement through your solicitors. This can include information on whether the property is owned equally or in unequal shares.

5. Understand your Inheritance Tax responsibilities

Cohabiting couples have no automatic right to inherit their partner’s estate. It’s worth researching how Inheritance Tax works. Cohabiting couples face the risk of ‘double taxation’, with Inheritance Tax payable upon the first and second death. It may be worth contacting an estate planner to prepare the optimal arrangement for your loved ones.

Related articles

Single vs joint life insurance

Types of life insurance

Do I need life insurance?

Life insurance when renting