Life insurance for renters

For millions of people, renting is a reality. And while many adults traditionally take out life cover when they get on the mortgage ladder, life insurance can also be an important consideration for renters, too.

You might also like...

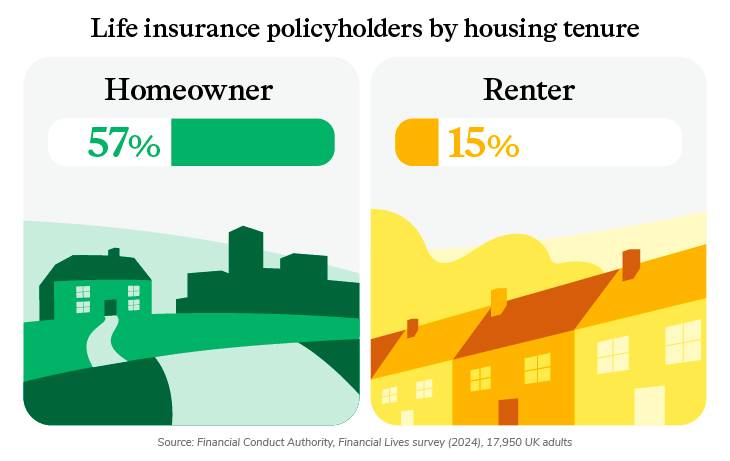

Whether you rent a property from a landlord, or you own your own home, life insurance can provide financial support to your family if you were no longer around.

Life insurance is designed to cover your life as an individual – or couple – rather than a property. So if you rent a property and you have financial dependants – such as a spouse, children or other family members – life insurance for renters can offer a lifeline.

Source: Financial Conduct Authority, Financial Lives survey (2024), 17,950 UK adults

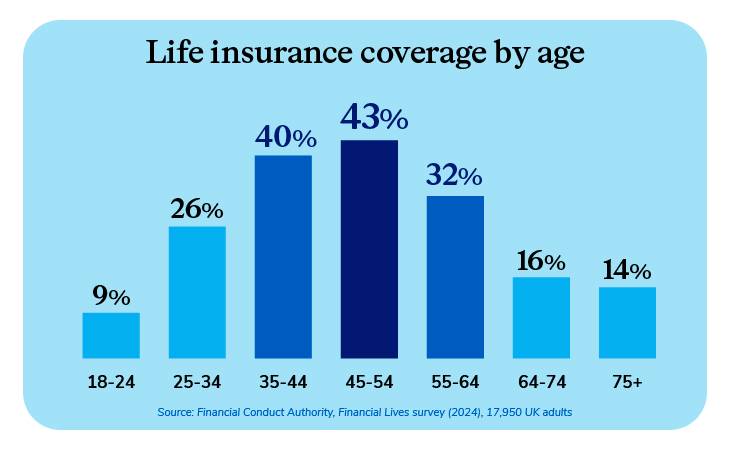

In particular, many younger adults lack the protection of a life insurance policy. Just 9% of 18-24 year olds have life insurance, rising to 43% among 45-54 year olds, according to the FCA survey.

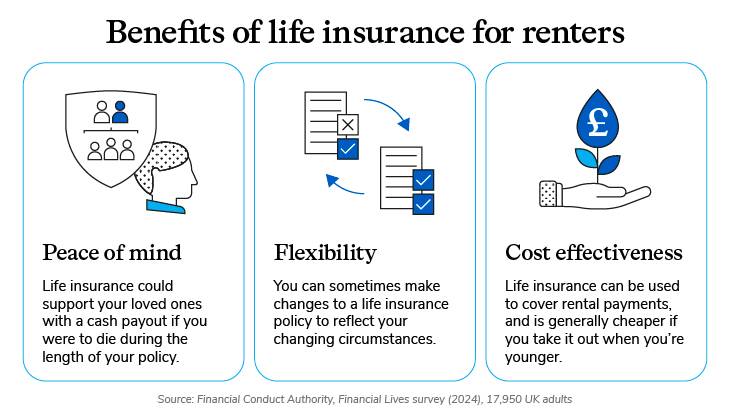

Benefits of life insurance for renters

- Peace of mind. Life insurance could support your loved ones with a cash payout if you were to die during the length of your policy.

- Flexibility. You can sometimes make changes to a life insurance policy to reflect your changing circumstances.

- Cost-effectiveness. A life insurance cash payout can be used for rental payments and is generally cheaper if you take it out when you're younger.

Types of life insurance for renters

Here are some life insurance options you might want to consider when renting:

Life insurance

If you die or you’re diagnosed with a terminal illness (life expectancy less than 12 months) during the length of your policy term, Life Insurance could pay out a cash sum. This could be used to cover the rent and bills while you're no longer around. Available from just £5 a month, depending on your circumstances and needs, so Life Insurance is worth considering for renters on a budget.

Single or joint life insurance

Couples in a rental accommodation may want to consider whether to take out single or joint life insurance; the former covers one person, whereas the latter covers two lives. Joint life insurance can be cheaper, but pays out upon the death of the first insured person (when the cover will stop) whereas two single policies ensures the surviving partner still has cover after the first death.

Critical Illness Cover

When taking out Life Insurance or Decreasing Life Insurance with L&G, you can add Critical Illness Cover for an extra cost. This optional cover could pay out a cash sum if you’re diagnosed with, or need a medical procedure for, one of the conditions covered by the policy during your policy term, and you survive for 14 days after diagnosis. Many people use this payout to help with everyday expenses such as rent, bills or financial commitments.

Want to learn more about Life Insurance?