What to do when a partner moves in

Every long-term relationship has significant milestones along the way, and moving in with a partner is certainly an exciting time. But aside from the novelty of living with your companion, there are various implications of cohabiting relationships to think about – from splitting bills to paying Council Tax. In this guide, we explain what to do when someone moves in with you.

Moving in with a partner who owns a house

Understandably, when moving in with a partner it’s much nicer to think about the positives, from spending more time together to hosting your friends and family. But equally, cohabiting relationships come with certain responsibilities, so it’s important to ensure you’re prepared for any worst-case scenario.

The legal definition of cohabiting

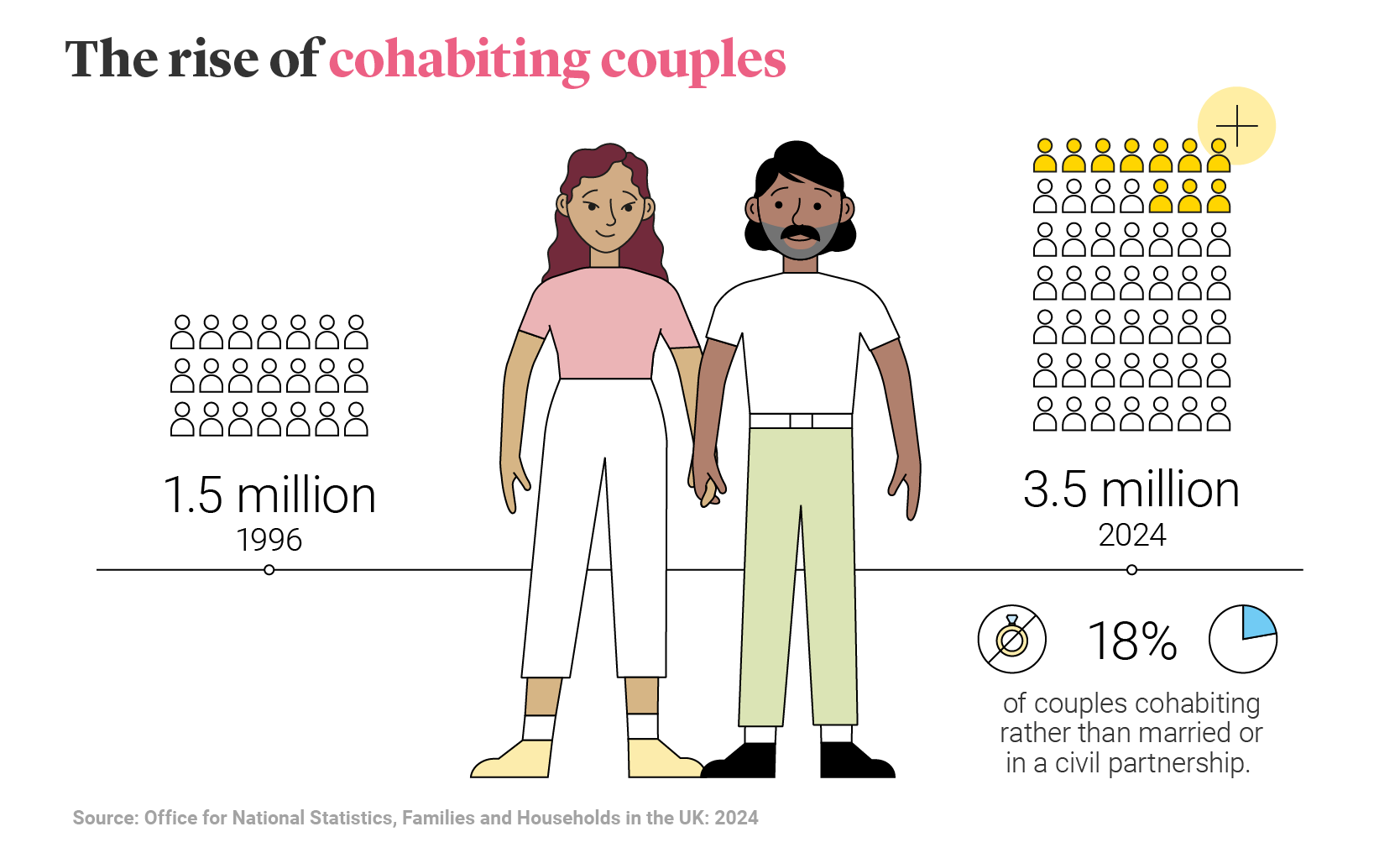

There is no legal definition of cohabiting, but it is generally understood to refer to couples that live together but aren’t married or in a civil partnership. It’s a common misconception that long-term cohabiting partners are in what’s known as a ‘common-law marriage.’

In the UK, cohabiting relationships don’t have the same rights as a married couple; for example, married partners automatically have the right to live in the ‘matrimonial home’.

How does a cohabiting relationship affect my rights?

If you are the property owner, you will retain your legal ownership of the home and any possessions that were bought before your partner moved in. However, if your partner is able to claim that they have a ‘beneficial interest’ in the property – for example, they may have contributed towards the mortgage – then theoretically they could force you to sell the property or claim proceeds from its sale.

What to do when someone moves in with you

There are no shortage of things to consider when moving in with a partner, so we’ve produced a checklist to help you get on top of that life admin and create a home sweet home.

- Discuss how you’ll split costs. Living together means you’ll have many shared expenses, from broadband and heating bills to paying Council Tax. In any cohabiting relationship, it’s important to decide how these costs will be split. You might want to go 50-50, but if one person earns much more than the other, this could get complicated (depending on your viewpoint). Whatever you decide, having an honest conversation is a good start.

- Consider a joint bank account. In a cohabiting relationship, you might find it easier to set up a joint bank account in both of your names, which you could use to settle shared costs like energy bills. But remember, both account holders will be liable for any debts accrued, so it’s really important that you and your partner are on the same page when it comes to your attitudes towards spending.

- Update your home insurance. If someone moves in with you, this can affect your home insurance premiums, as your insurer will base any payout on the number of people living at a property, and (for contents insurance) the value of possessions like laptops or jewellery. In terms of how to declare a partner moving in, you should contact your insurer with information about who will be occupying your home.

- Consolidate existing expenses. Now that you’re living together, you won’t need to be paying two lots of bills for certain outgoings, such as your TV licence, utilities, home insurance or Council Tax. Make sure that any unnecessary Direct Debit payments have been cancelled so you’re not out of pocket.

- Think about life insurance. If you own a property with a partner and one of you were to die while covered by the policy, a life insurance payout could help the surviving partner pay for the mortgage. And life insurance isn't just for homeowners– if you rent together, could your partner manage financially if you were to pass away?

What is classed as living together for benefits?

No two households are exactly the same, and if you’re in receipt of benefits, knowing what to do when someone moves in can seem complicated at first. Your entitlement to benefits changes according to whether the Department for Work and Pensions (DWP) classifies you as a single adult, single parent, or living as part of a couple. For example, you won’t be able to claim for Universal Credit as a couple if you have joint savings or capital of over £16,000.

As far as the DWP are concerned, the legal definition of cohabiting applies to couples who are living in the same household and are any of the following:

- Married

- In a civil partnership

- “Living together as though [you’re] married”.

This last definition of cohabitation can cause confusion; for example, you may have a partner who often stays over but lives in a separate household. If you’re in this situation, it’s a good idea to ensure that you and your partner retain documentation – such as a driving licence or car registration – that shows you live at different residences. This could prove useful if you’re contacted by the benefits office to prove your household status.

How to declare a partner moving in

There are various scenarios where you might wish to declare that a partner has moved in with you. For example, you can contact your local authority when someone moves in so that you pay the correct amount of Council Tax.

If you’re in receipt of benefits such as Universal Credit and a partner moves in, you can report a change of circumstances by signing into your Universal Credit account.

Moreover, if you’re a parent, you may be able to receive Child Tax Credit for a maximum of two children per household, although there are exemptions for some larger families. If you’re unsure about what your family are entitled to, you can contact the Child Benefit Office to enquire, or report a change to your circumstances if a partner moves in.

Want to learn more about Life Insurance?

Other related articles

Single vs joint life insurance

Changing Life Insurance Policy

How to keep your house warm in winter

Putting life insurance in trust

Life insurance and tax