Putting life insurance in trust

Writing life insurance in trust is one of the best ways to protect your family’s future in the event of your death. Your life insurance policy is a significant asset. By putting life insurance in trust you can manage the way your beneficiaries receive their inheritance. Here, we take you through the benefits of life insurance trusts, how the process works, who’s involved and the other considerations.

You might also be interested in...

What is a trust?

Trusts are a straightforward legal arrangement. They let you leave assets to friends, relatives or whoever you pick to be your beneficiaries. A trust is managed by one or more trustees – family members, friends, or a legal professional – until the trust pays out to your beneficiaries. This can either happen upon your death, or on a specified date such as when a child turns 18.

Your life insurance policy can be put into a trust, which is often referred to as ‘writing life insurance in trust’. One of the main benefits of this approach is that the value of your policy is generally not considered part of your estate.

How does putting life insurance in trust work?

You will need to decide which type of trust is right for you. Your options are:

- Discretionary Trusts – your trustees have a high level of discretion about which beneficiaries to pay when you’re no longer around, using your letter of wishes as a guide. Your letter of wishes outlines your intentions as to how trustees should administer the trust.

- A Flexible Trust - is a trust where there are two types of beneficiaries. The first type of beneficiary is the default beneficiary. These beneficiaries are entitled to any income from the trust as it arises. In practice, if the life policy is the only asset in the trust there will not be any income. The second type of beneficiary is the discretionary beneficiary. These discretionary beneficiaries only receive capital or income from the trust if the trustees make appointments to them during the trust period. If no appointments are made by the end of the trust period, the default beneficiaries will receive all the benefits.

- Survivor’s Discretionary Trust – this form of joint life insurance in trust pays out to the surviving policy owner. For example, if you die before your partner, they would be entitled to inherit your policy before your beneficiaries. If both policy owners die within 30 days of one another, your beneficiaries can benefit on the same basis as a Discretionary Trust.

- Absolute Trust – in this scenario, the beneficiaries are named individuals who cannot be changed in the future. This includes any children born later and a spouse following a divorce. The advantage of an Absolute Trust is that the pay-outs can be made quickly without long legal delays. As with other trusts the Inheritance Tax is likely to be nil or negligible.

Once your trust is set up, your trustees legally own the policy and must keep the trust deed safe – they can ask a solicitor to store the documents or find a safe place in their home. Your trustees will ultimately make a claim to your insurer when you pass away, so they will need the trust deed close to hand.

It’s worth remembering that as the settlor, you maintain responsibility for making sure your life insurance premiums are paid. It may be beneficial to hire a legal adviser to ensure the legal wording of your trust agreement is precise.

Who can be a beneficiary?

You can choose any person, or people, to be your beneficiaries - this will entitle them to receive a pay out in the event a valid claim is made. Contrary to what some people may assume, there are no rules that restrict who your life insurance beneficiary can be. For example, you could choose the following:

While you won't be able to change your beneficiaries if you have an Absolute Trust, if you take out a Discretionary Trust, your trustees will have the freedom to decide who your beneficiaries are, and how much they're entitled to receive from a pay out.

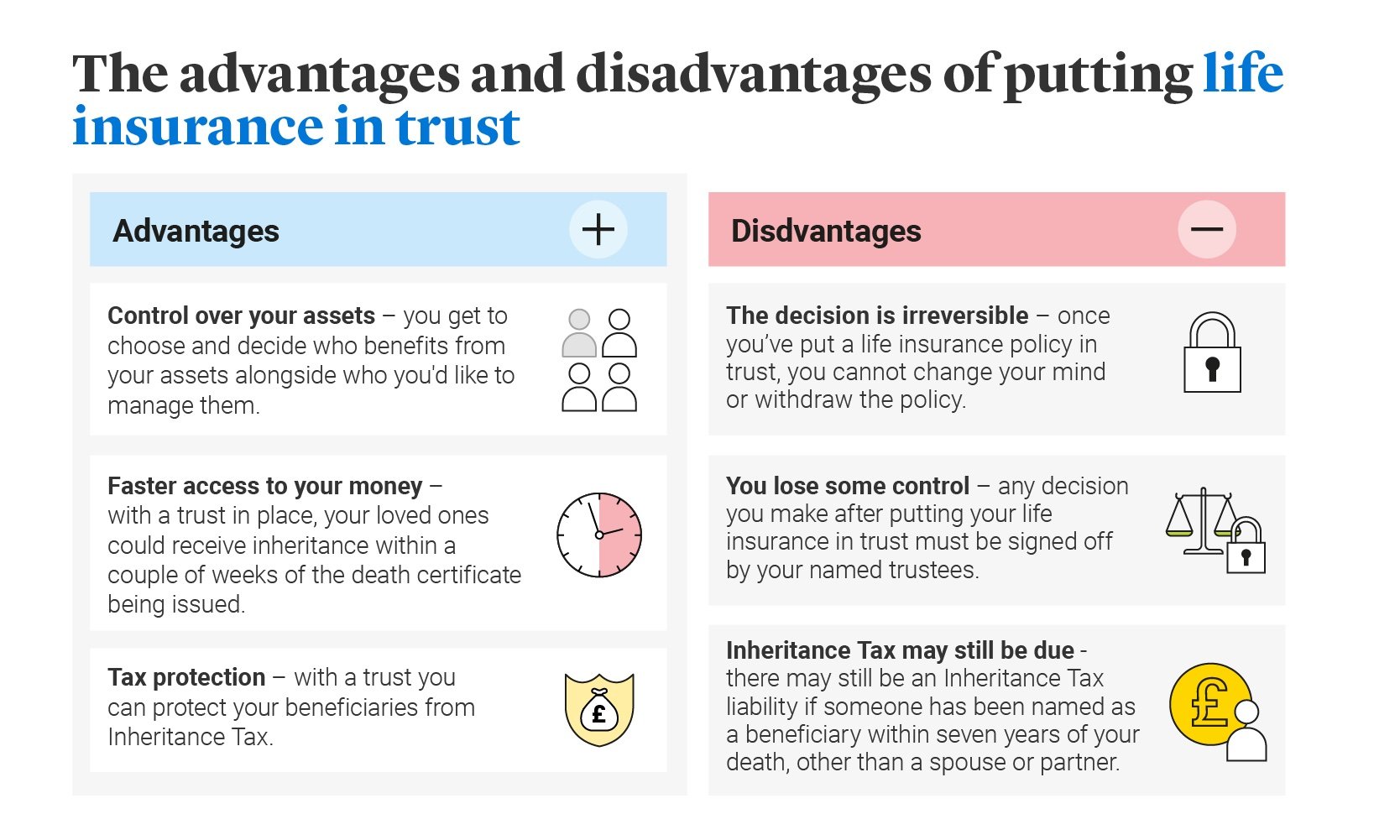

The benefits of writing life insurance in trust

There are many reasons why putting life insurance in trust is a popular option. Here are some of the ways you can benefit from a life insurance trust.

- Control over your assets – if you don’t have a trust, your money might be used to pay off outstanding debts. Putting life insurance in trust gives you greater discretion, as you can decide who to appoint as your beneficiaries and trustees. Setting up a trust is especially important if you’re not married or in a civil partnership, as otherwise, your assets may not transfer to the intended recipient.

- Faster access to your money – without a trust, when you die your would-be beneficiaries would need to obtain probate, which can cause delays. With a trust in place, your loved ones could receive the inheritance within a couple of weeks of the death certificate being issued. You can read more in our guide to the probate process.

- Protect your beneficiaries from Inheritance Tax – writing life insurance in trust means the money paid out from your policy should not be considered part of your estate. There are exceptions; for example, you may be liable for an Inheritance Tax charge on the value of the property on each ten-year anniversary. Currently, the standard Inheritance Tax rate is 40%, which is charged on the part of your estate above the £325,000 threshold.

Disadvantages of putting life insurance in trust

While there are benefits to putting life insurance in trust, what about the downsides?

- The decision is irreversible. Once you’ve put a life insurance policy in trust, there’s no turning back. You’ll be unable to withdraw the policy as the decision will be considered irrevocable.

- You lose some control. Once your life insurance is in trust, any decision must be signed off by your named trustees, not just yourself.

Life insurance in trust for cohabiting couples

According to ONS data, the population who are cohabiting is growing. In 2022 22.7% of the population aged 16 years and over were cohabiting compared with 19.7% in 2012.

While there is no legal definition of a cohabiting couple, sometimes called common-law spouses, it generally means to live together as a couple without being married. However it’s a misconception that common-law spouses have the same legal rights as a married couple, or as couples in a civil partnership.

The truth is that there are no cohabiting rules in law, and a surviving co-habitee has no legal claim on their deceased partner’s estate unless they left a will that includes their co-habiting partner. And, if a life insurance policy is not written in trust, they will have no legal claim on the policy either.

If you are living together without marriage or civil partnership, it’s even more crucial that you have clear legal and financial protection in place for your partner and children after you die. With a life insurance policy written in trust, the proceeds of the policy can be paid directly to your intended beneficiaries, rather than to your legal estate.

Joint life insurance in trust

A joint life insurance policy covers both partners but pays out only once in the event of a valid terminal illness or death claim. This is usually after the first death, with the intention to financially support the surviving partner.

Once the policy has paid out, it ends, leaving the surviving partner without life insurance cover under the policy. If both partners die at the same time, then the lump sum would be paid to the estate of the younger of the life assured.

If the policyholders are co habiting, then the surviving partner receives the lump sum but for IHT calculations, half the cash sum is deemed to form part of the deceased’s estate. This is not normally an issue for married or civil partnerships.

With a joint life insurance policy, there is still a benefit in putting the policy into trust, especially if you are not legally married or in a civil partnership. For a married couple, life insurance policies include an inheritance tax exemption for the spouse or civil partner, but this doesn’t apply if you have a joint policy and are cohabiting.

If you place your policy into a Discretionary Survivor Trust, the trustees can pay any money to the surviving partner as long as they're still alive 30 days after the death of their partner.

If the surviving partner dies within 30 days of the other partner, the trustees can pay the money straight to the beneficiaries of the Trust (for example, your children or grandchildren). This way, the beneficiaries usually won’t pay Inheritance Tax on the money as part of either yours or your partner’s estate.

Married or cohabiting couples can choose to take out a single life policy each, a joint policy that provides cover for both partners, or a combination of both. A single policy covers one person, and when that person dies the policy pays out a lump sum to their estate. If a couple have a policy each, the policies remain completely independent of each other and can be for different amounts or with different companies, and each one pays out when the policy holder dies.

Please remember, life insurance is not a savings or investment product and has no cash value unless a valid claim is made.

How long does a trust last?

Technically, your trust can last up to 125 years – there is no expiry date for trusts set-up for charitable purposes – but ultimately, your trust agreement should last however long you deem necessary. Your personal circumstances may influence the length of time you stipulate; for example, the trust could last until a child grows up and marries.

Is there an extra cost?

There is no added cost to putting life insurance in trust with Legal & General. You can put your personal life insurance policy in trust when you take it out, or at any time after that – you simply need to own the policy. You should note that if you transfer your life insurance policy to another individual, this may have implications for your trust so it’s best to contact us directly or seek legal advice.

Want to learn more about Life Insurance?

You may also wish to explore Over 50s Life Insurance

Related Articles

Who should be your life insurance beneficiary?

What you need to know if you’re a life insurance beneficiary

Life insurance and tax

Protecting yourself from life insurance scams

How do life insurance payouts work?